A review of external economic and property market factors influencing urban planning

In this VPA Research Quarterly

The property market appears to be moderating following a period of high activity levels, however the alignment and delivery of planning activities, infrastructure co-ordination and development remains a challenge across Government and the development industry following a period of prolonged peak demand. In this Research Quarterly we cover:

• Victorian growth and economic overview

• Construction activity

• Regional growth

• Greenfield market update

Section 1: Victorian Growth and Economic Overview

• The Victorian economy and particularly the property and planning sectors have remained buoyed throughout the COVID-19 period with strong levels of housing and land demand while higher density products have remained more challenged, this is despite declining population.

• Confidence in the property sector will likely subdue through 2022 with activity levels moderating, continued increasing costs, supply chain challenges and interest rate rises.

• Planning can support economic growth and recovery via optimising supply levers, however demand and infrastructure challenges will continue to become more apparent in light of tighter budgetary constraints.

Economy / Labour Force

• Economic recovery and performance in Victoria continues to gain momentum.

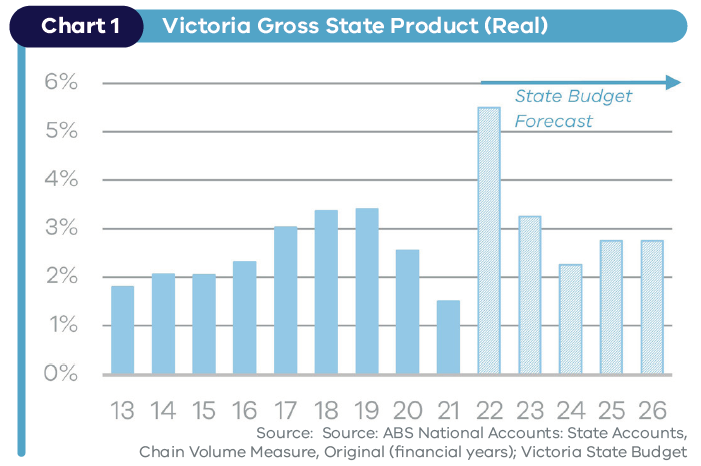

• Following a modest -0.4% contraction in 2020/21, the latest State Budget is forecasting a strong bounce back of 5.5% for GSP in 2022/23 then follow prepandemic levels (Chart 1).O

• Despite the expected recovery, total debt is projected to grow from $102b currently to $168b by 2025/26, when the annual budget is expected to return to surplus. Budget repair will be a key focus for many years to come.

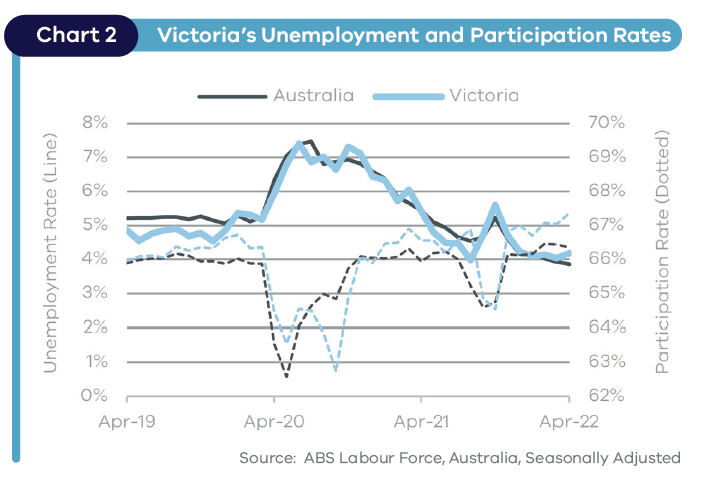

• Unemployment increased slightly to 4.2% in April ’22, but remains significantly lower than the 5.6% recorded six months ago. The current rate is historically low and not expected to hold outside the short term.

• Labour participation has lifted and at over 67% is now exceeding the national average (Chart 2).

Population Growth

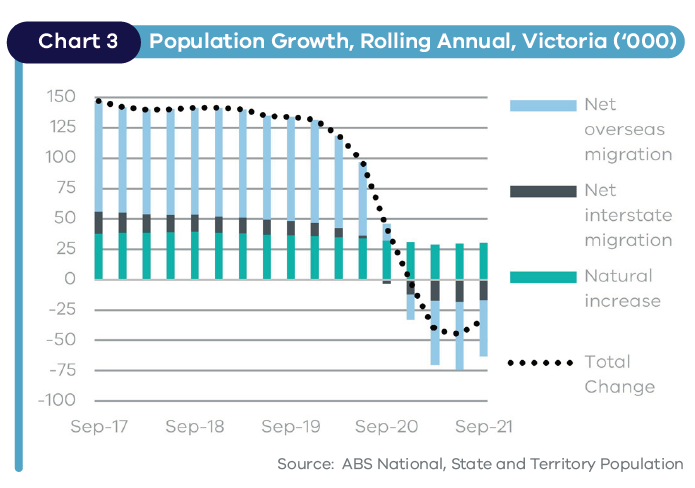

• Victoria’s population continues to decline, although the rate of decline has eased slightly as net overseas migration begins to recover (Chart 3).

• Victoria lost a total of 6,000 residents for the September quarter 2021.

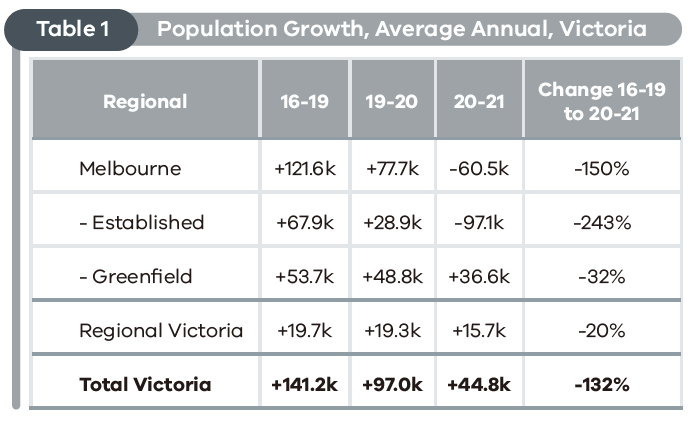

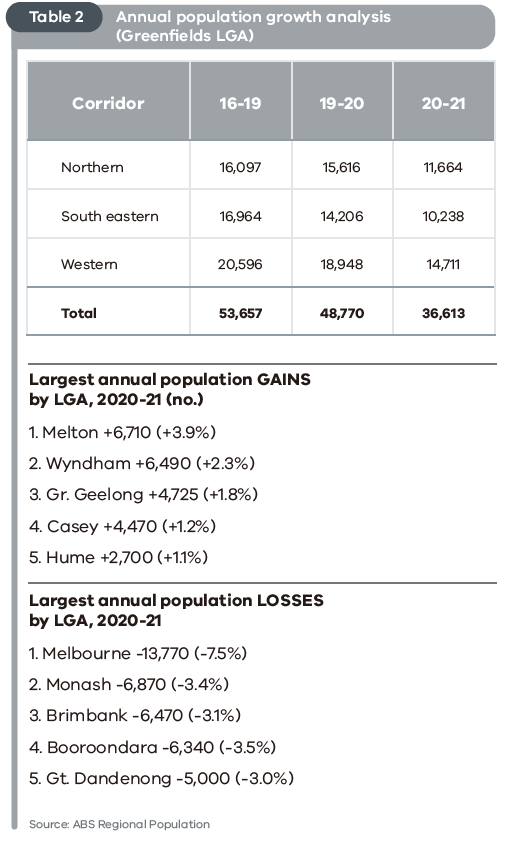

• Throughout 2020-21, Victoria’s population losses were largely centred in Melbourne’s established suburbs which decreased by -97,100 people (Table 1).

• Melbourne’s greenfield growth areas increased by +36,600 and Regional Victoria increased by +15,700.

• The latest State Budget anticipates that population will stabilise in 2021-22 (+0.1%) and recover to +1.7% by 2023-24.

Housing Market

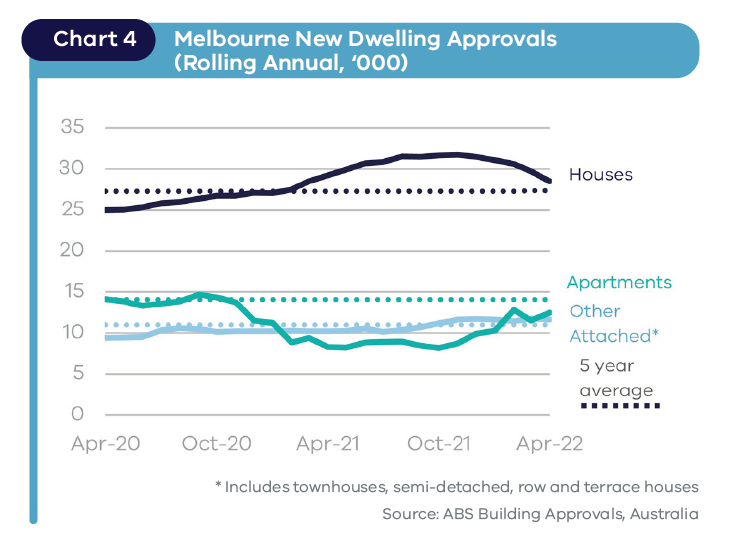

• Throughout the COVID-19 period, detached dwellings continued to perform strongly and observed activity levels above prevailing levels (Chart 4).

• While apartments and higher density product declined during the COVID-19 impact period, New Dwelling Approvals (NDAs) have started to increase in 2022.

• More than 4,300 NDAs were granted in established suburbs in February (73% total Melbourne), which was the highest monthly figure recorded since November 2017.

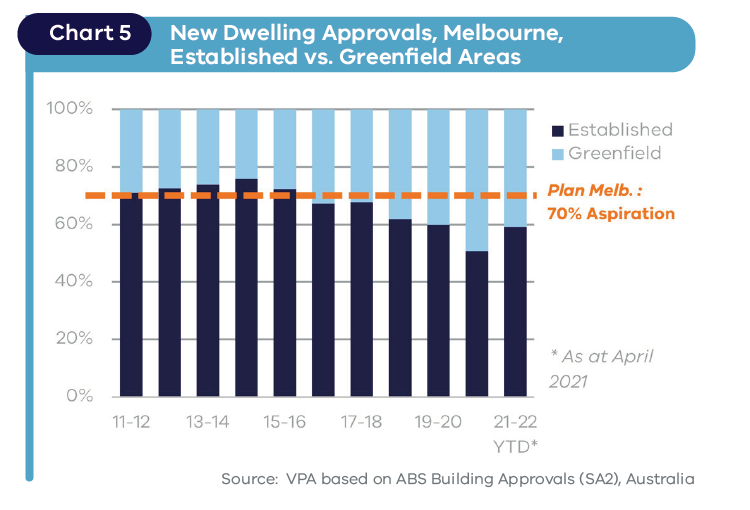

• The recent increase in metropolitan approvals, and particularly higher density approvals, has supported an improvement in progress towards Plan Melbourne’s established and greenfields 70/30 Population Growth aspiration. (Chart 5).

Section 2: Population Growth & Migration

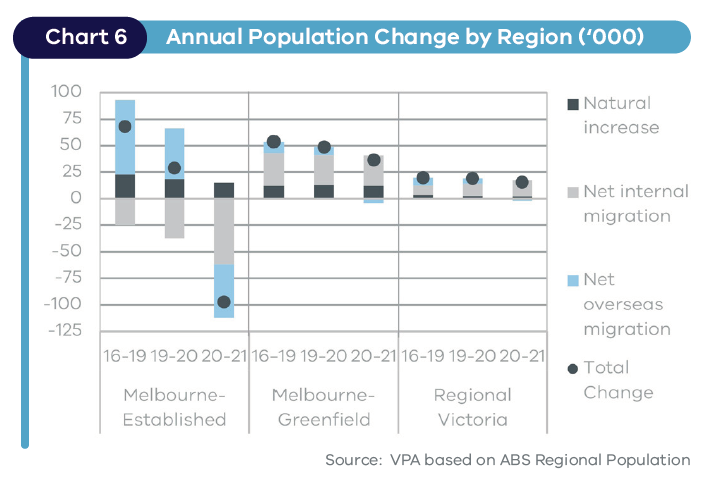

• Regional Victoria and greenfield growth areas maintained similar levels of population growth to pre-COVID-19 levels, with only minor reductions driven by Net Overseas Migration (Chart 6).

• Regional growth occurred in areas in close proximity to Melbourne (within two hours commute), growing by an average 1.8% p.a. from 2019-2021, compared with just 0.3% p.a. for the balance of the regions.

• A significant population decrease is evident in established Melbourne, most notably in LGA’s of Melbourne, Monash, Brimbank and Boroondara.

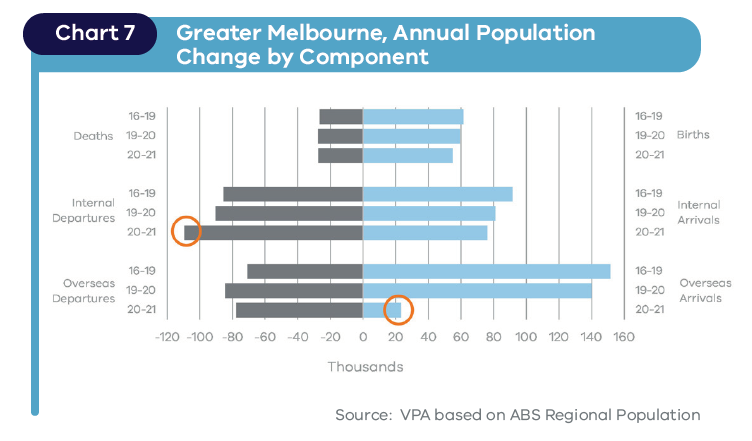

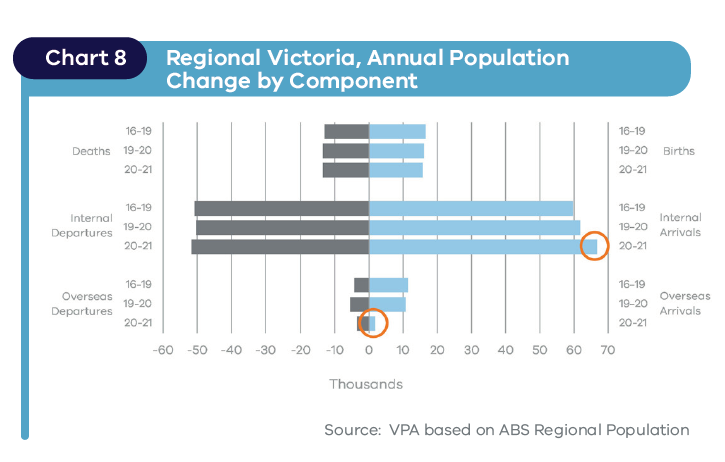

• Total internal movements remained robust, with a spike in internal departures from metropolitan areas and a corresponding spike in internal arrivals to the regions (Chart 7 and Chart 8).

Section 3: Regions continue robust growth with some supply challenges emerging

• Many property and demographic commentators suggest there is a regional renaissance or surge of population growth to the regions. Whilst regional areas have held strong throughout the COVID-19 period, the total numbers are not significant at a state level. However, areas experiencing existing housing shortages are being further challenged.

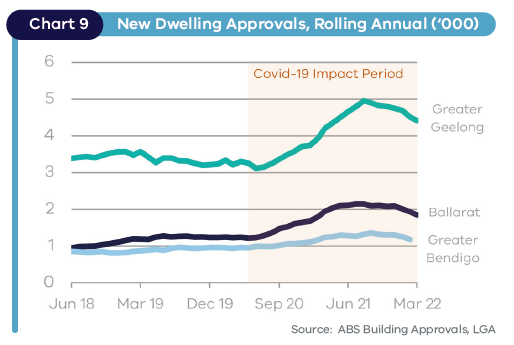

• Ballarat, Bendigo and Geelong represent the vast majority of growth in regional Victoria, accounting for 44% of total approvals on an annual basis, or around 7,400 approvals (Chart 9).

• Whilst the increase in activity within Ballarat, Bendigo and Geelong represents a 27% increase, this represents a relatively small increase of 2,000 dwellings for the years across the three cities, relative to the state that records 69,000 NDAs per annum. However, where zoned land supply is limited, particularly in Ballarat and Geelong, this presents a more pressing challenge.

• In the January 2022 Research Quarterly we outlined the Urban Development Program status of key regional cities prepared by the Department of Environment, Land, Water and Planning (DELWP), with Ballarat and Geelong both having around 7-9 years land supply available or less given recent demand increases.

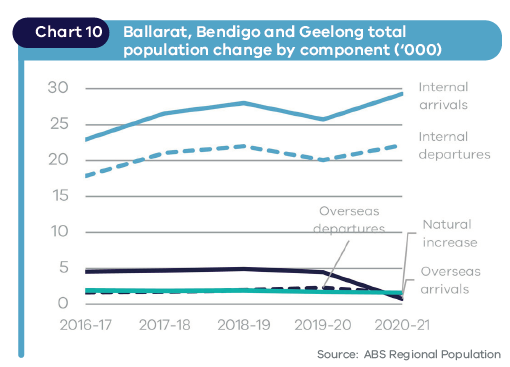

• The source of total population movements including natural increase, Net Internal Migration (NIM) and Net Overseas Migration (NOM) (Chart 10) highlight NIM to Ballarat, Bendigo and Geelong has increased in the COVID-19 impact period, with internal arrivals increasing at a faster pace than departures.

Section 4: Construction Activity

Crane activity

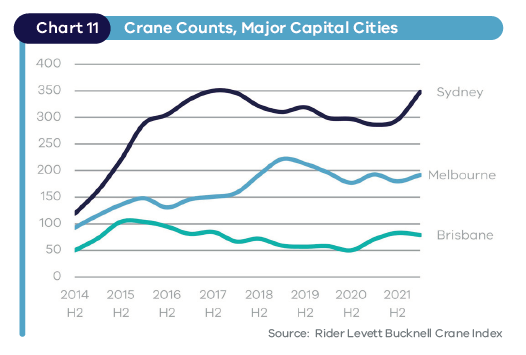

• Crane activity across Melbourne has remained relatively steady with a total of 192 cranes currently active.

• The majority of cranes (some 47%) are located in inner city areas, noting that historically inner areas have accounted for 60%+ of crane activity (Chart 11).

• This highlights the continued emergence of larger scale and higher density construction projects in middle and outer suburbs, in addition to supporting major civic works.

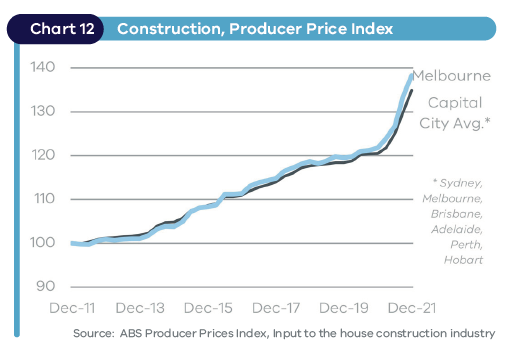

Rising construction costs continue to plague the housing industry. The ABS recently reported growth of more than 15% in construction costs in the past year (Chart 12), on the back of:

• higher material costs, including timber, board and joinery (+21%) and ‘other metal’ products (+16%)

• labour shortages

• supply chain constraints.

In Melbourne, cost growth has slightly exceeded the capital city average. Cost is expected to remain a key issue for the property sector this year in line with current uncertainty around global disruptions.

In addition to cost increases, supply chain impacts are also delaying development timeframes, further placing development cost pressures.