So how long will this downturn cycle continue?

Currently I see a window of opportunity for property investors with a long-term focus.

This window of opportunity is not because properties are cheap, however, when you look back into three years’ time the price you would pay for the property today will definitely look cheap.

The opportunity arises because consumer confidence is low and many prospective homebuyers and investors are sitting on the sidelines.

However, I believe later this year or early next year as many prospective buyers will realise that interest rates are near their peak, inflation will have peaked and the RBA’s efforts will bring it under control.

And at that time pent-up demand will be released as greed (FOMO) overtakes fear (FOBE – Fear of buying early), as it always does as the property cycle moves on.

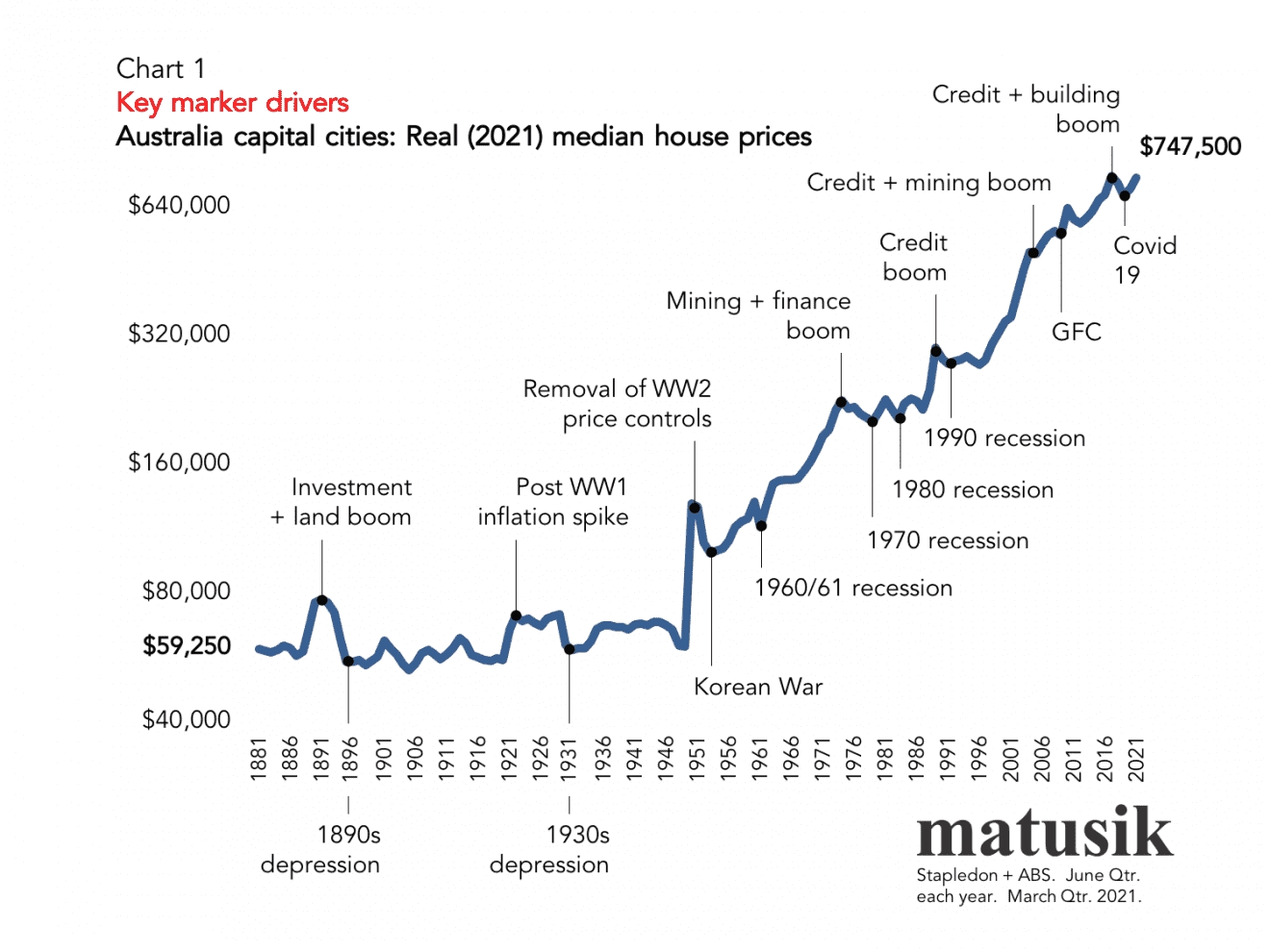

We saw an opportunity like this in late 2018 – early 2019 when fear of the upcoming Federal election stopped buyers from entering the market. And look what’s happened to property prices since then.

I saw similar opportunities at the end of the Global Financial Crisis and in 2002 after the tech wreck. History has a way of repeating itself.

You see…consumer sentiment shifts play a big role in the world of property.

When consumer sentiment is low as it currently is, this shows up in various metrics including:

- Rising days on market (how long it takes to sell a property.

- Property sales volumes reducing

- Vendor discounting increasing to meet the market

- Auction clearance rates falling

- Prices at the premium end of the property market fall first.

But as consumer sentiment picks up, and it will once people realise inflation has peaked and the RBA doesn’t need to increase interest rates further, and that’s likely to be in the first or second quarter of 2023, we’ll see a shift in the metrics

- Buyers will feel more confident and re-enter the market.

- Property prices will stop falling

- More vendors will feel comfortable putting their properties up for sale.

- Prices will stabilise for a while and then slowly pick up

- The media will start telling good news stories, rather than trying to scare us about real estate Armageddon

Poor consumer sentiment when most other economic fundamentals are strong simply means it’s a cloud covering the sun.

Spring will follow Winter, and Summer will follow Spring – this too shall pass by and the long-term upward trend of the value of well-located properties will continue.

So my recommendation is that if you’re in a financially sound position, to buying while others are sitting on the sidelines

While it may feel strange and counterintuitive to buy in a correcting market, there are many valid reasons why this is the best time to buy….and history has shown this to be correct over and over again.

- There is less competition at present.

- You have more time to conduct your due diligence and research.

- It’s a buyer’s market that gives you the upper hand in negotiations.

But don’t try and time the market – this is just too difficult.

And don’t look for a bargain – A-grade homes and investment-grade properties are in short supply and still selling for reasonably good prices.

These high-quality properties will tend to hold their value far better than B and C-grade properties located in inferior positions and inferior suburbs.

And don’t worry too much…

While a lot has been said about the +20% increase in property values many locations have enjoyed prior to this downturn, it must be remembered that the last peak for our property markets was in 2017 and in many locations housing prices remain stagnant over a subsequent couple of years which means that average price growth was unexceptional over the long term, averaging out at around 5 per cent per annum over the last 5 years.

Now I know some people are worried and wondering: “Are the Australian property markets going to crash in 2022 0r 2023?”

They hear the perpetual property pessimists who’ve been chasing headlines and telling everyone who’s prepared to listen that the Australian property markets are going to crash and housing values could drop up to 20% – but just look at the terrible track records – they’ve been predicting this every year for the last decade and they’ve been wrong.

What is really affecting the market currently is poor consumer confidence.

What drives Australian property prices?

As we discussed earlier, there isn’t ‘one’ Australian property market.

In fact, there isn’t even just one Melbourne, Sydney, Brisbane etc. property market either.

Every market in every area is segmented, and prices in some of these segments will outperform going forwards, while others will not.

But forecasting Australian house prices isn’t as simple as it might seem.

In the medium term, property values will be linked to the extent that our economic recovery affects income, employment, borrowing capacity, and credit availability.

Generally, this boils down to two basic economic concepts: Supply and demand, and inflation.

However, there is a sub-component of demand, called “capacity-to-pay”, which is often overlooked.

Understanding how these concepts work together to affect real estate is crucial to one’s belief or doubt about whether real estate values will rise.

In a free-market economy, prices of any commodity will tend to drop when supply is high and demand is low.

In other words, when there is more than enough of something, it is said to be a “buyer’s market” because sellers must compete, typically by lowering the price, to attract a buyer.

Conversely, when supply is low and demand is high, prices will tend to rise as buyers bid up pricing to compete for the limited supply. This is called a “seller’s market”.

Let’s look at it this way….

- With regard to supply…. they aren’t making any more real estate in the most desirable areas and by this, I’m talking about the dirt, not the buildings.

- With regard to demand, Australia has a business plan to increase the population to 40,000,000 people in the next 30 years.

Now we’ve covered the two basic economic concepts, let’s take a look at the 8 key underlying fundamentals supporting our property markets in the medium-long term.

1. POPULATION GROWTH

For the last few decades, continued strong population growth has been a key driver supporting our property markets.

Australia’s population was growing by around 360,000 people per annum, meaning we needed to build around 170,000-180,000 new dwellings each year to accommodate all the new households.

Over the last two years, population growth stagnated, but this should increase again now that the gates have been opened and over 200,000 overseas immigrants will be allowed to come to our shores.

Of course, Australia is likely to be seen as one of the safe havens in the world moving forward.

At the same time, the number of new properties listed for sale in our capital cities is falling creating an imbalance of supply and demand.

2. HOUSING SUPPLY

Housing supply clearly has a significant influence over house prices: an undersupply puts pressure on prices to rise while an oversupply would do the opposite.

The oversupply of dwellings previously experienced in many Australian locations has now disappeared and there are very few new large development projects on the drawing board.

We’re experiencing a severe undersupply of well-located properties in our capital cities and considering how long it takes to build new estates or large apartment complexes, and because of increased construction costs, most developments on the drawing board are not financially viable at present, meaning there is no suggesting we’ll have an oversupply of properties for some time.

3. HOUSE SIZE TRENDS HAVE CHANGED

Also on the topic of supply, Australian households have aged and pretty soon millennials will make up one-third of the property market and their household trend, in general, is for smaller-sized properties.

More one and two-person households mean that moving forward, we will need more dwellings for the same number of people.

4. INTEREST RATES

A low-interest-rate environment makes it possible for buyers to borrow more money, and more cheaply.

This in turn, as we saw over the past couple of years, creates a headwind for buyers.

More buyers mean supply struggles to catch up, and an imbalance occurs.

In the current market, interest rates are rising quickly, and are expected to hike further throughout the remainder of the year, but the peak of interest rates is in sight with the RBA now slowing the level of its interest rate hikes.

5. RENTERS

Increased rental demand at a time of very low vacancy rates will see rentals continue to rise for the next few years.

And this will put pressure on the housing supply.

Soon 40% of our population will be renters, partly because of affordability issues but also because of lifestyle choices.

The government isn’t providing accommodation for these people. That’s up to you and me as property investors.

On the other hand, the pressurised rental market will force some would-be buyers to get into the property market sooner than planned.

6. INVESTORS

Investors help drive market sentiment and trends, which has a knock-on effect on property prices.

Despite the recent rise in interest rates, investors are back with a vengeance.

Some are attracted by the rising rents and higher yields, while others are taking advantage of the window of opportunity the current buyer’s market is offering.

More investors mean more buyers, which means more demand versus the supply of properties available.

7. THE ECONOMY

Another key factor that affects the value of the property market is the overall health of the economy.

This is generally measured by economic indicators such as the gross domestic product (GDP), employment data, manufacturing activity, the prices of goods, etc.

Broadly speaking, the economy is strong and the RBA is trying to slow it down to bring inflation under control, but currently, everybody who wants a job can get a job and this will underpin our housing markets even if the economy falters a little moving forward.

8. AVAILABILITY OF DEBT

It goes without saying that the availability of debt directly affects the trajectory of property prices.

At the moment, Australia’s banking system is strong, stable, and sound.

And the banks are trying to attract new customers with honeymoon interest rate deals.

Even though a few home buyers have overcommitted themselves financially, there should be no real concern about household debt because, in general, it is in the hands of those who can afford it.

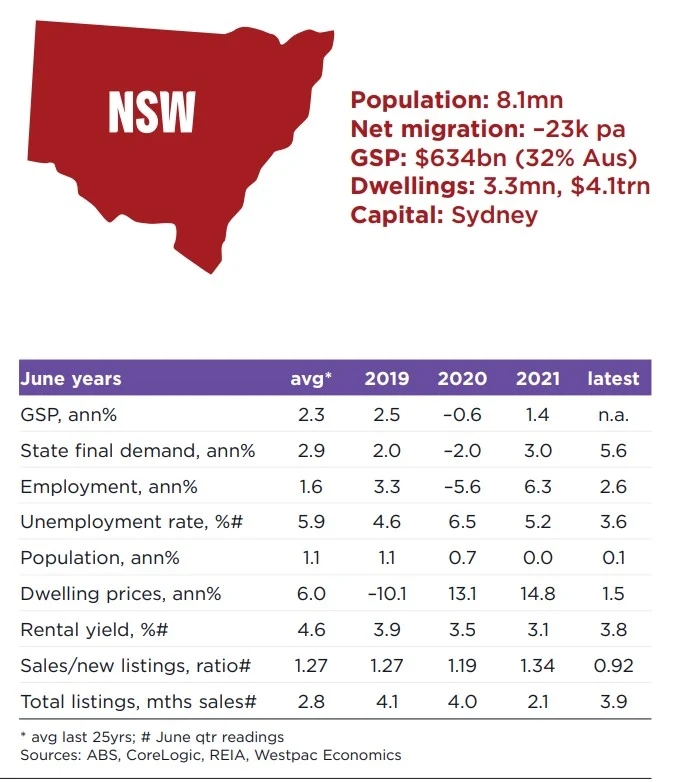

Sydney House Price Forecast

Australia’s house prices reached record highs during the peak of the Covid-19, with our most expensive city – Sydney – leading the pack.

And while prices have since cooled from their peak across the city, Sydney’s property market continues to fetch impressive prices, particularly in some of the most sought-after areas.

After all, some of the city’s suburbs are so tightly held lithat an available property for sale comes around once in a blue moon with homeowners holding onto their houses for as long as 20 years.

And areas in lifestyle or coastal suburbs are still in particularly strong demand as homebuyers wait to secure their dream property.

The city’s median price for houses now stands at $1.257 million, down 6.1% since the last quarter and down 9.3% over the year.

It’s a similar story for units which have fallen 3.3% over the quarter and 6.8% over the year to a new $783,406 median.

As the market cools, the number of home sales has fallen and over the last few months Sydney auction clearance rates have been rising, indicating more buyers and sellers are reaching an agreement on price.

At Metropole Sydney we’re finding that strategic investors are looking to take advantage of the window of opportunity currently available to them, while homebuyers are still actively looking to upgrade, picking the eyes out of the market.

While overall Sydney property values are likely to fall further over the rest of the year, like all our capital cities there is not one Sydney property market, and A-grade homes and investment-grade properties remain in strong demand are likely to outperform, many holding their values well.

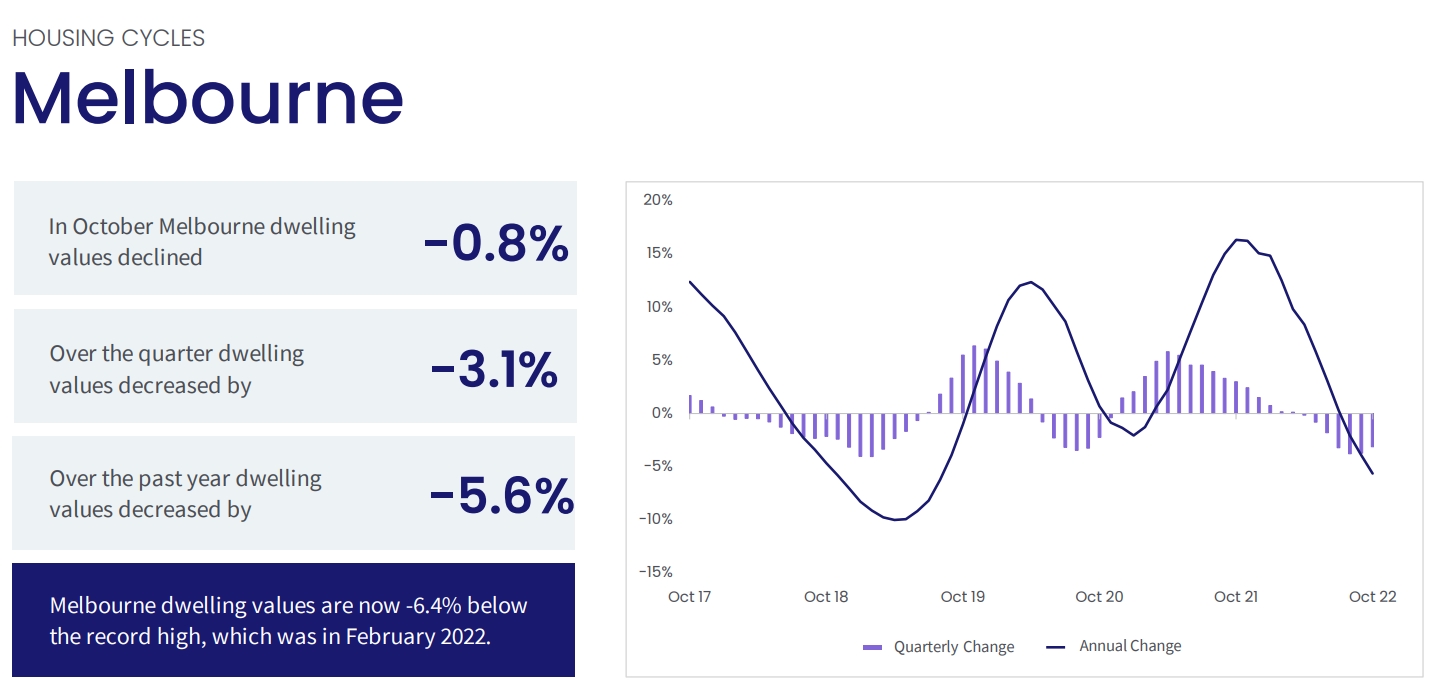

Melbourne House Price Forecast

Housing values across Melbourne increased by 17% through the growth phase, with house values up 21% and unit values rising 11%.

Since peaking in February, house values are down -3% and unit values have reduced by -1%.

Taking the recent decline into consideration, Melbourne housing values are up by 8.6% or roughly $24,200 since the onset of Covid back in March 2020.

As conditions cool, the number of home sales is also trending lower, down by an estimated -18% in the June quarter compared with the same period last year.

As buyer demand wanes, advertised supply levels have risen to be 3% higher than a year ago and 9% above the five-year average for this time of the year.

With more stock, market conditions are now favouring buyers over sellers with clearance rates holding below 60%, while days on market and vendor discounting rates trended higher for private treaty sales.

With higher inventory levels and less competition, buyers are gradually getting some leverage back.

At Metropole Melbourne we’re finding that strategic investors and homebuyers are still actively looking to upgrade, picking the eyes out of the market.

While overall Melbourne property values are likely to fall further over the rest of the year, like all our capital cities there is not one Melbourne property market, and A-grade homes and investment-grade properties remain in strong demand and are likely to outperform, many holding their values well.

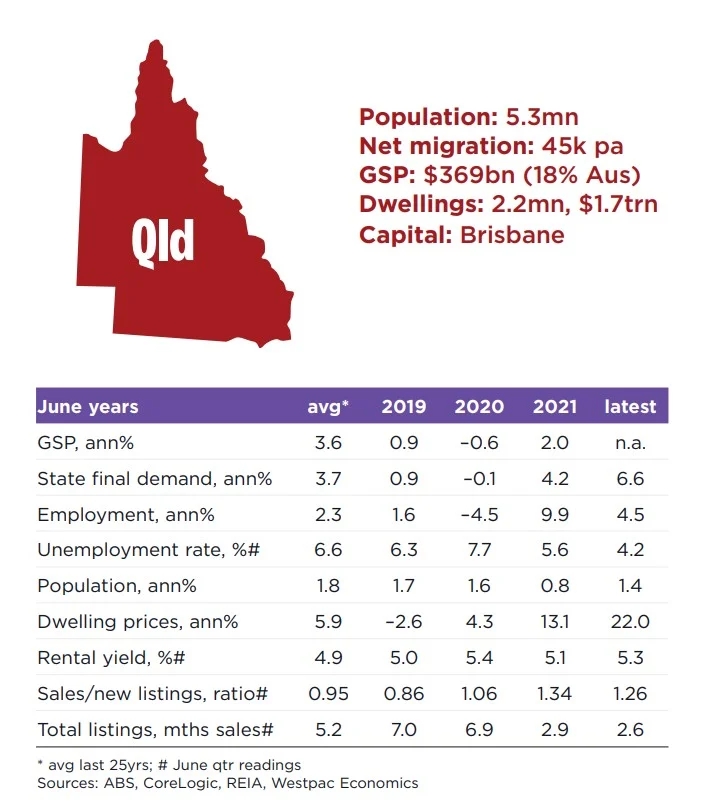

Brisbane House Price Forecast

Brisbane’s house prices saw the steepest annual climb in 13 years in 2021, as the city’s property market came to grips with relentless Covid-19-induced demand for property.

This once-in-a-generation property boom resulted in almost 400 suburbs joining the million-dollar club.

And even as growth slowed in other parts of Australia, Brisbane’s housing market continued to perform strongly in the first half of 2022.

Even though prices have now begun to fall from their peak, the market has done so with a significant lag from the price drops across the rest of Australia.

And unlike in Sydney and Melbourne, prices are still far higher across the city than just 12 months ago.

As of November, the median price for houses in Brisbane stood at $817,684, which is a 2.2% decline month-on-month and a 6.2% decline quarter-on-quarter.

But year-on-year, Brisbane’s house prices are 8% higher today.

It’s the same story for units too.

Brisbane’s $494,785 median unit price is 0.9% lower than last month, 1.2% lower quarter-on-quarter but still a 10.7% improvement on prices recorded at the same time last year.

Why is the market so robust, you might ask?

Well, there has been significant internal migration (particularly northwards from Victoria and NSW) into Queensland with Australians looking for more affordable property in lifestyle suburbs.

And the property market is prosperous as a result.

But even though the north-eastern state remains one of the country’s most robust, if you’re looking to buy, you’ll be pleased to hear that you can get more bang for your buck in Brisbane compared to Sydney and Melbourne.

Currently the team at Metropole’s Brisbane office are finding property investor activity to be strong, particularly for houses, and not only coming from locals but from interstate investors who see strong upside in Brisbane property prices as well as favourable rental returns.

However, there is not one Queensland property market, nor one southeast Queensland property market, and different locations are performing differently and are likely to continue to do so.

Houses remain a firm favourite of prospective home hunters, with demand rising post-lockdown and it remains significantly elevated compared to last year.

However, apartment demand has been sliding and, in general, apartments in Queensland are a higher risk investment than houses, particularly due to a high supply of apartments that are unsuitable for families or owner-occupiers.

Brisbane is likely to be one of the best performing property markets over the next few years, but while some locations in Brisbane have strong growth potential, the right properties in these locations will make great long-term investments, and certain submarkets should be avoided like the plague.

Our Metropole Brisbane team has noticed a significant increase in local consumer confidence with many more homebuyers and investors showing interest in a property.

At the same time we are getting more enquiries from interstate investors there we have for many, many years.

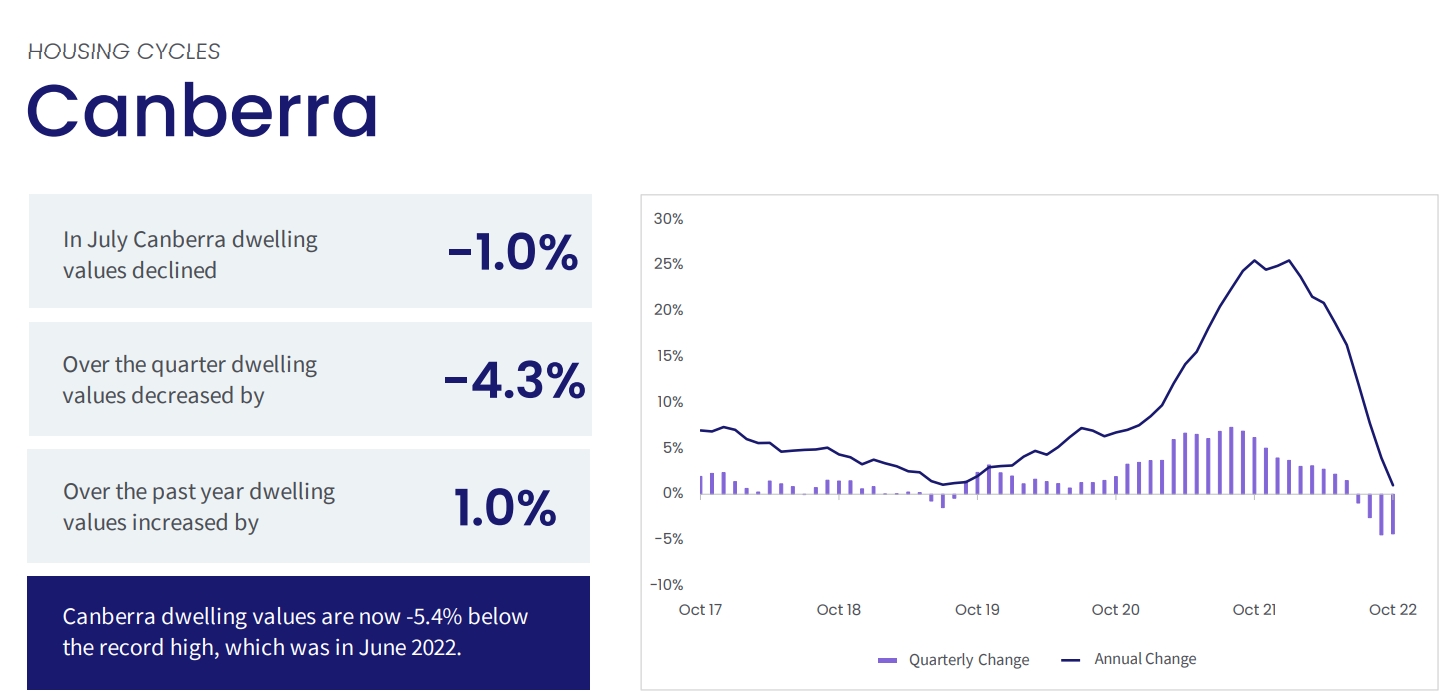

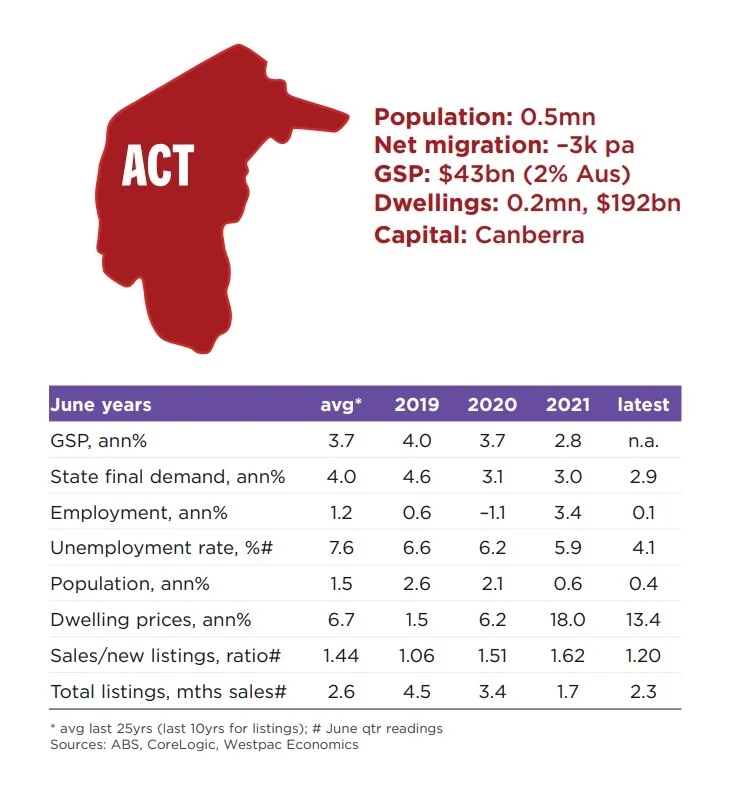

Canberra House Price Forecasts

Canberra’s property market has been a “quiet achiever” with median house prices recording the biggest jump in prices across all of Australia’s capital cities, at a huge 25.5% in just one year or 3.7% over the quarter, to a new median of $1.015 million according to Domain’s House Price Report.

That means that prices soared by almost $1,054 a day over the June quarter to give a total rise of $96,000.

This is the steepest price acceleration in almost three decades, the Domain report explained.

Median house prices in the inner north, inner south, and Woden Valley are now all above seven digits.

But unit price growth has been more restrained as the development boom of recent years contains prices, although they are edging closer to a record high, up a more modest $18,000 (or 3.6%) over the June quarter to $504,217.

Interestingly, since the pandemic, Canberra house prices have risen a huge 30.9% and unit prices 9.4%, which is the highest rate of growth across all of Australia’s cities.

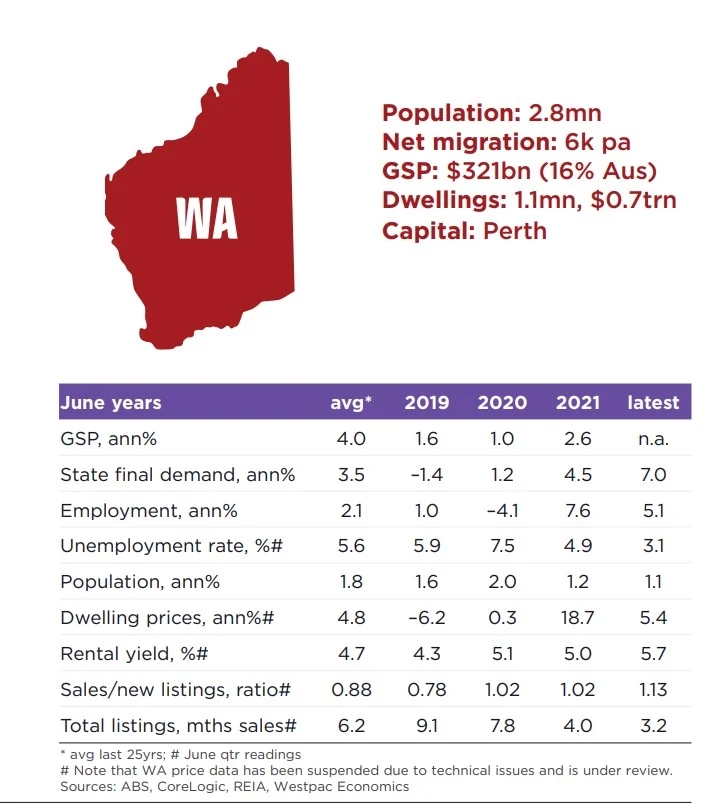

Perth House Price Forecast

Perth housing values were up 0.4% in June, marketing the second month in a row where the rate of capital gain has reduced.

The slowdown follows a temporary rebound in Perth’s rate of growth that coincided with reopened state borders, however, it is looking like the Perth market is once again losing some steam alongside the national trend.

Advertised housing stock remains extremely low and is trending lower as buying activity remains elevated, implying selling conditions remain strong across the Perth market.

This is backed up by rapid selling times as homes average just 18 days to sell, although such rapid selling time has occurred as discounting rates have edged higher.

With the median dwelling value of $558,600 remaining the lowest across the capital cities, housing affordability is less challenging than in other capitals, which could help to insulate the Perth housing market from a larger downturn.

Perth’s isolation and economic over-reliance on the mining industry mean many potential home buyers would look at moving away to further their careers.

But the attractive property prices in Western Australia do not mean that investors should jump into the Perth property market – there are better opportunities in other parts of Australia.

The problem is the Western Australian economy is too dependent on one industry – the mining industry and much of this is dependent on China, and this has a direct knock-on effect on Western Australian house prices.

Without structural changes to the WA economy, it is unlikely to be able to deliver the significant number of higher-paying jobs and the substantial increase in population growth required to keep driving strong housing price growth in the medium to long term.

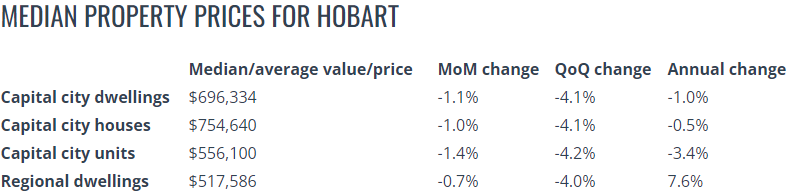

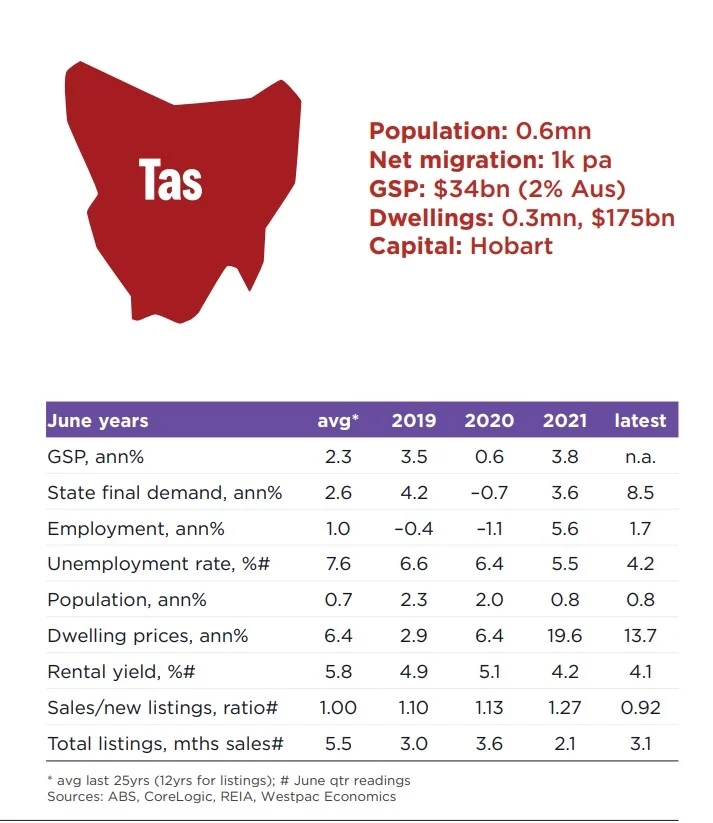

Hobart House Price Forecast

Hobart was the darling of speculative property investors and the best-performing property market in 2017-8, but since then Hobart property growth has slowed.

Hobart property prices have been supported by strong demand and weak market supply.

Here we have pulled together the latest data on Tasmania’s property prices.

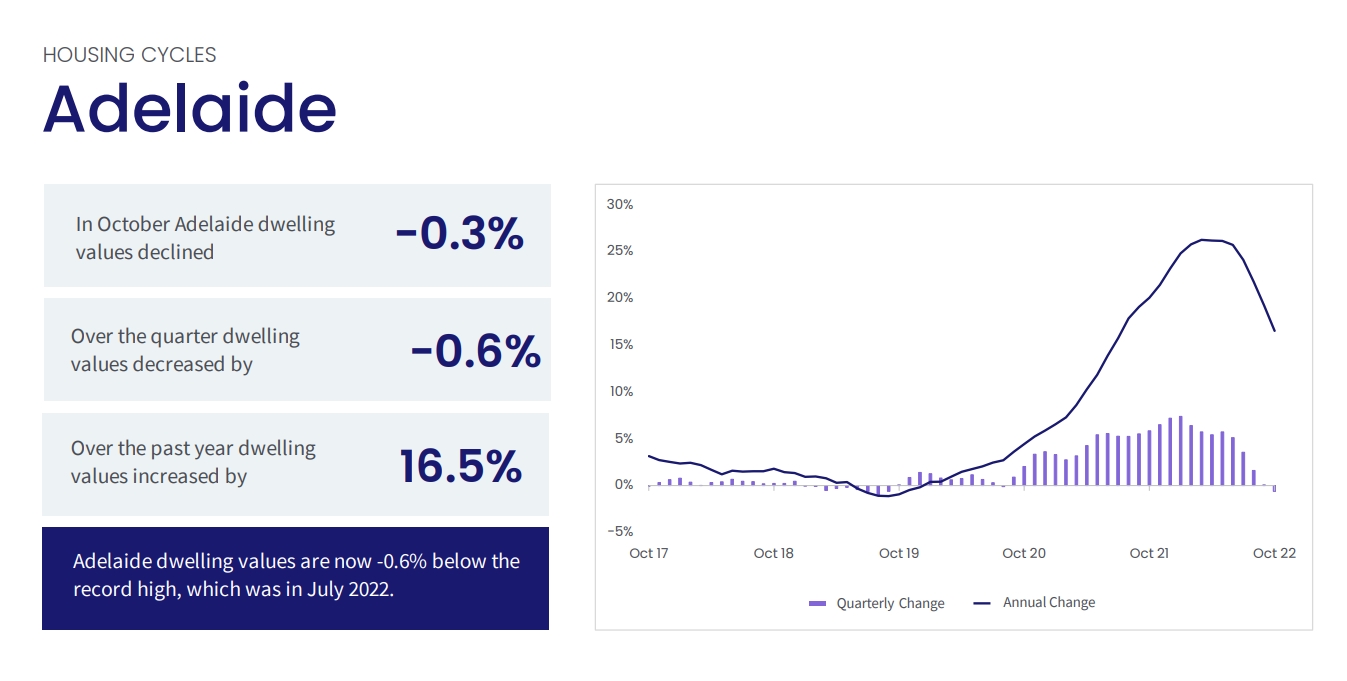

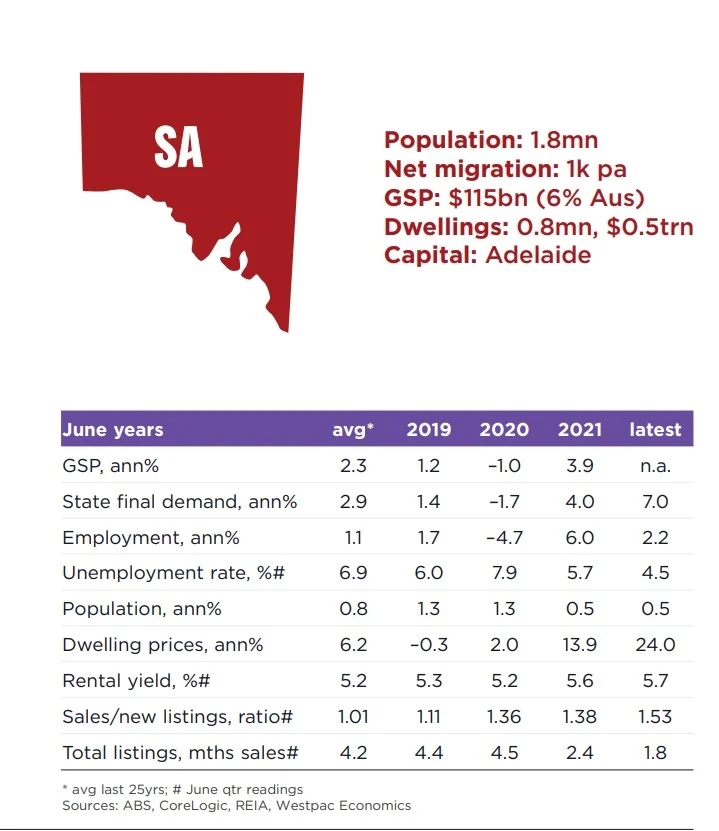

Adelaide House Price Forecast

Adelaide has continued to stand out as the nation’s strongest capital city housing market.

Through the growth cycle, Adelaide housing values have increased by 44% adding roughly $197,000 to the median dwelling value.

Most of this growth has been centred in the housing market rather than units, with values up 48% through the cycle to date, while unit values are up a smaller 23%.

One of the key factors pushing up prices is the ongoing shortage of advertised supply.

However the Adelaide property market has now joined the rest of Australia in its housing slowdown falling 0.2% in the last month, but still up 44.2% since the pandemic began in March 2020.

Long-term prospects for Australian property markets (2025-2030)

With property values rising by more than 20% in most locations around Australia during the boom of 2020-21, affordability started to bite, particularly in lower socio-economic areas and in our two big capital cities.

As I have already suggested moving forward our housing markets will be fragmented as certain demographic segments will find the rising cost of living due to inflation and higher rents or higher mortgage costs at a time when wages are not keeping up with inflation will either stop them getting into the property markets or severely restrict their borrowing capacity.

Currently, there are about 26 million Australians and Australia’s population is forecast to rise to 29 million people by 2030.

This means 3 million more people will need somewhere to live and this will underpin our property markets

In early 2021 the Government released the Intergenerational Report (IGR) to help Australia and the businesses plan for the next 40 years.

The IGR projects an Australian population of 38.8 million by 2060-61, and even though this is a little lower than previous projections – due to Covid slowing things down – this still means Australia’s population is projected to grow faster than most other developed countries.

Despite the reduction of the projected population, these trends are truly monumental.

If you think about it, it’s taken Australia well over 200 years since European settlement to reach a population of 25.5 million people today.

But in the next 40 years, our population will increase by around 13.3 million people.

In other words, it will increase by over 50%!

To make this worse, currently, there are 2.5 people in each household, but the IGR forecasts the average number of people in each household will shrink a little moving forward, meaning we are going to require about a third more real estate than we currently have.

To deal with the projected population growth between now and 2061 it’s likely we’re going to require one new property built for every two properties that currently exist!

All this means our way of living is going to change considerably and town planners will struggle to cope with this growth.

So when we think about the real estate forecast for the next five years in Australia, we have to think about how population growth will impact property investment choices.

And how strategic, knowledgeable investors will be well-placed to capitalise on the changing trends.

What we predict for Australia’s property market is that there will be many more high-rise towers of apartments, not just in the CBD but in our middle-ring suburbs.

In fact, we are already starting to see this, particularly in Melbourne and Sydney.

And we also expect there will be lots more medium-density housing – in particular townhouses will be a popular way to live with modern large accommodation on more compact blocks of land.

Great, so what are the predicted house prices in 2030 Australia?

It would be foolish to try to forecast property prices moving forward because no one really knows what’s going to happen to inflation and interest rates.

But what we can see is that as more of us want to live in the large capital cities of Australia (and in particular in those locations close to the CBD or the water) where there will be more manatees, and the scarcity will only push the price of properties upwards.

Other questions I often get asked

IS THERE A PROPERTY BUBBLE IN AUSTRALIA?

This question was commonly asked last year when we were in a property boom and some so called “experts” were warning that we could be in a property price bubble about to burst.

But, there’s a huge difference between property booms and price bubbles.

Bubbles invariably bust and when they do, housing prices end up much lower than where they started.

Property booms on the other hand, eventually run out of steam with an occasional small price correction followed by a prolonged period of little to no growth.

The issue is that they both look the same at the start.

So what’s the difference between a boom and bubble?

It’s the type of buyers causing the growth.

Buying demand from investors grows when prices rise and the more that they increase, the more that investors want to buy properties.

Whereas owner-occupier booms take place despite price growth and the more that prices rise, the more that demand slows down and then stops as prices become unaffordable.

Only investor led booms can become bubbles.

Investor led booms can become bubbles because investors don’t buy properties to live in, like owner-occupiers do.

Profit is their only consideration, and fear of loss their only concern.

This means that when price growth slows down or stops, investors start to put their properties on the market and try to sell.

When the number of properties for sale exceeds buyer demand, prices start to fall.

Panic starts to set in as more and more investors try to sell and because no one wants to buy, the bubble busts.

SO, ARE WE IN A PROPERTY BUBBLE?

No.

Because the property boom seen in 2020-21 was a result of buyers taking advantage of extremely low interest rates and government incentives designed to keep our economy afloat amid a slowdown.

These were mainly owner-occupier buyers looking to upgrade their existing property or even those looking to jump on the property ladder sooner than planned to take advantage of the cheaper borrowing costs.

This was not an investor led speculative bubble.

Owner-occupier booms merely slow down and when they end prices don’t crash, because the purchased properties are now people’s homes.

When buyer demand comes to an end, there’s no motivation to sell.

Only those homeowners who really need to move for personal, family or business reasons will do so.

Property booms can occur anytime and anywhere that the demand for housing outpaces the supply, but only investor led booms can turn into bubbles (but usually don’t).

SHOULD I BUY A HOUSE NOW OR WAIT UNTIL 2023 OR 2024?

For some of you who are reading this right now, 2023 will absolutely be the worst possible time you could consider buying a property.

There is the spectre of higher interest rates, the continual media coverage predicting falling property values and an imminent property crash (which by the way is wrong) and geopolitical tensions around the world.

In fact for some people, moving forward with a real estate purchase this year would have the potential to cripple them financially, not just now but well into the future.

But the reality is that for investors, there is no ‘best’ or ‘worst’ time to buy property.

Here’s why…

Property investment is a process, not just an event.

So rather than just talking about going out and buying a property in 2023, or how to time the market to best purchase a property, the right time for you to consider investing is when you have all your ducks in a row and it suits your finances and your long term plans.

This means you have:

- A strategic property plan, so you know where you’re heading and what you need to do to achieve your financial goals,

- Set up the right ownership structures to protect your assets and legally minimise your tax,

- A robust finance strategy with a rainy day buffer in place to buy you time

IS IT WORTH BUYING A HOUSE IN AUSTRALIA?

In terms of capital growth, it might not have the speed of crypto or stocks, but in terms of delivering consistent results over time, Australia’s real estate is a spectacular investment.

Australia’s property market has consistently delivered results over time.

In fact, Australia’s property boom saw 5 Aussie cities placed in Knight Frank’s global top 20 for prime property price growth in 2022.

International property consultancy Knight Frank’s Prime Global Cities Index Q1 2022, crowned the Gold Coast as Australia’s top-ranking prime property market thanks to robust property price growth.

The city ranked in 7th place with a 19.3% annual hike in prime property prices.

Sydney came in close behind in 9th place with a 16% increase in prices while Brisbane and Perth came in 12th and 13th place with respective 11.3% and 11% increases.

Melbourne also made the top 20 list in 14th place with a 10.9% annual price growth.