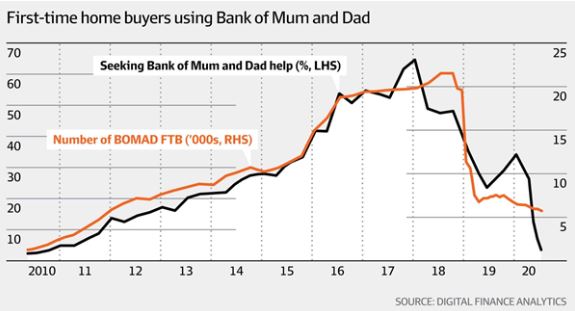

Lending institutions and consultants said that “parents’ banks” (buying homes funded by their parents) are making a comeback, due to new low lending rates, generous government incentives for first home buyers, and reduced competition from investors, which has increased parental assistance The pressure of children owning their own property. Digital Finance Analytics (DFA), which monitors the loan market, pointed out that after the general election in May last year, the loans for parents to support their children reached a peak, but then such loans dropped from about 12,000 per month to just over 1,200.

Many banks have implemented stricter mortgage terms to match the Banking Code issued at the end of June last year.

For example, the loan guarantors of the National Australia Bank (NAB) face more stringent scrutiny. They must provide information on how the loan will affect their financial situation, and they must understand that if something goes wrong, they may need to pay off their debt. The Commonwealth Bank of Australia (CBA), the country’s largest lending institution, said it would assess the work or income of the guarantor and would not accept the guarantor’s main residence as a guarantee if their income mainly comes from pensions.

The bank will not consider the income of the guarantor when considering whether the customer is capable of repaying the loan, and there is a three-day “cooling-off period” to encourage the guarantor to seek independent legal and financial advice.

In addition, banks that offer the lowest interest rates usually require a higher loan-to-value ratio, usually around 70%, rather than the 80% required by most banks. Steve Mickenbecker, executive officer of the Canstar Group, which monitors fees and interest rates, said: “As the recession approaches, risk awareness of mortgage lenders will increase, and they will more strictly review income security when evaluating loans.”