Where to from here?

We saw an uptick in auction volumes as sellers raced to market in a pre-Easter Super Saturday surge. More homes went to auction than any other week so far this year.

But for the rest of April, both buyers and sellers may perhaps be less active as we navigate the Easter break and Anzac Day. Then there’s the upcoming federal election to contest with.

It could be that much of the activity we have seen to date is fuelled by an urgency to transact before the election and rate rises.

Looking ahead, there are headwinds that will continue to slow housing prices from the surge recorded over the past year, given the benefits of lower mortgage rates have already been converted into higher prices. The average rate on new mortgages has risen since last year and housing affordability will worsen as repayments become more expensive with rising interest rates.

Search volumes continue to slip as market activity moderates

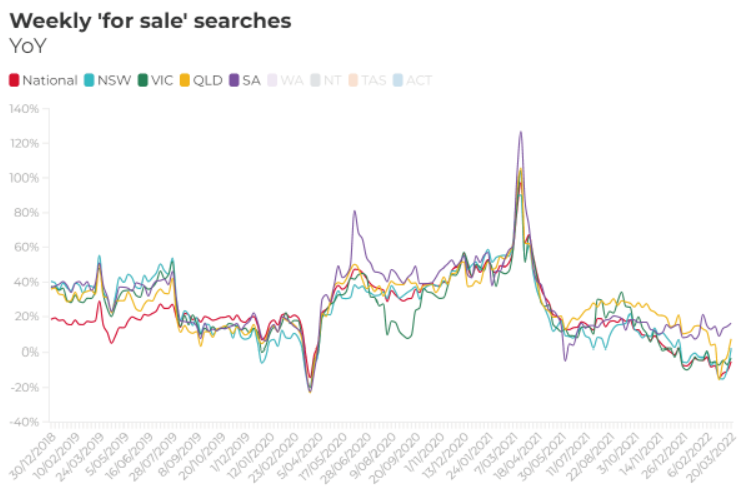

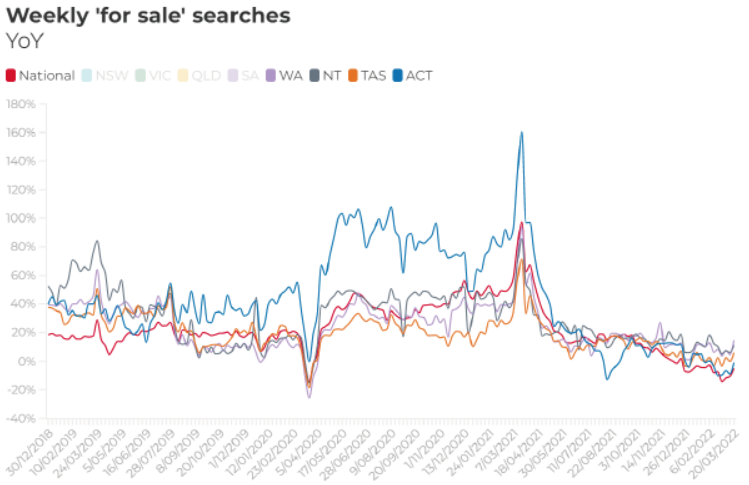

Australia-wide, search volumes in March 2022 fell 8% month-on- month from February and 11% year-on-year from March 2021.

On a monthly basis, search volumes have dropped off in every state by varying amounts. The largest monthly declines in search volumes have been experienced in Queensland (down 15%) and New South Wales (down 11%). There is likely to have been some disruption to search volumes in March due to the severe flooding that has affected the east coast, as well as holiday long weekends in Victoria, South Australia, the Australian Capital Territory and Tasmania.

On an annual basis, search volumes are also lower in some states compared to March 2021. Year-on-year search volumes have declined the most in NSW (down 10%), ACT (down 7%), and Victoria (down 5%). When compared to March last year, search volumes remain higher in WA (13%), SA (7%), and the Northern Territory (7%).

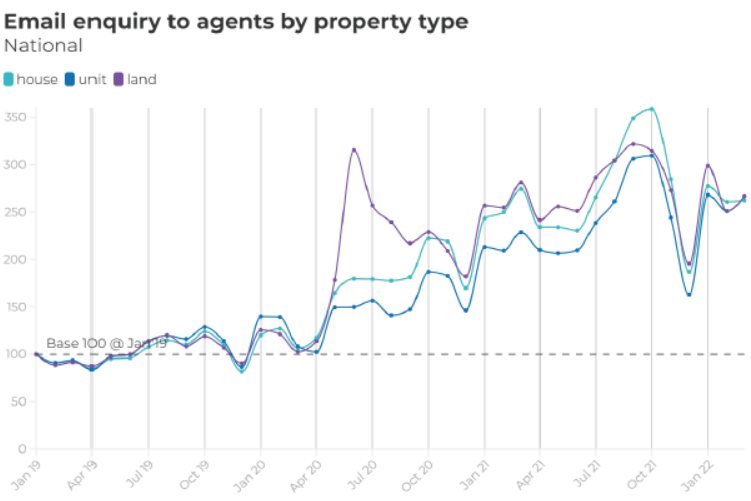

Unit enquiry makes a comeback

Enquiry on realestate.com.au for properties for sale hit a record high in October 2021. Since then, as COVID-19 restrictions have eased – meaning prospective buyers can view homes unencumbered – the number of email enquiries to real estate agents on realestate.com.au has fallen sharply from 2021’s elevated levels.

This lower level of email enquiry volume has continued into March. Since last year’s peak, the volume of email enquiries to real estate agents across all property types on realestate.com.au has fallen 22.1%.

Although, in March 2022, each property type recorded a monthly increase in enquiries from February’s levels across houses (0.6%), units (6.2%) and land (6.3%). Overall, enquiry volumes for all property types rose 2.8% month-on-month and remain 1.5% higher than March last year.

Here, it’s the volume of unit enquiry that’s keeping overall enquiry volumes elevated compared to the same time last year. Enquiry volumes for both houses (down 4.4%) and land (down 5.1%) have slipped relative to March 2021, but the volume of unit enquiry is 16.6% higher year-on-year.

With search and enquiry volumes easing and HomeBuilder having ended, it wouldn’t be a surprise to see a further decline in vacant land enquiry, given that many prospective buyers have now purchased, and housing construction costs are becoming more expensive.

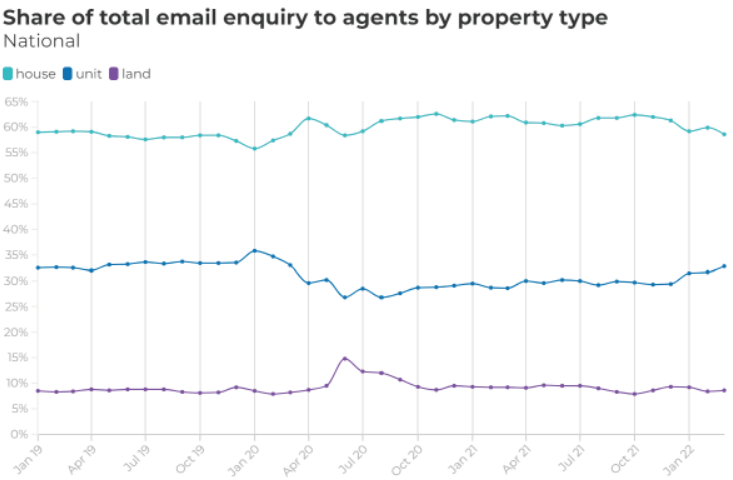

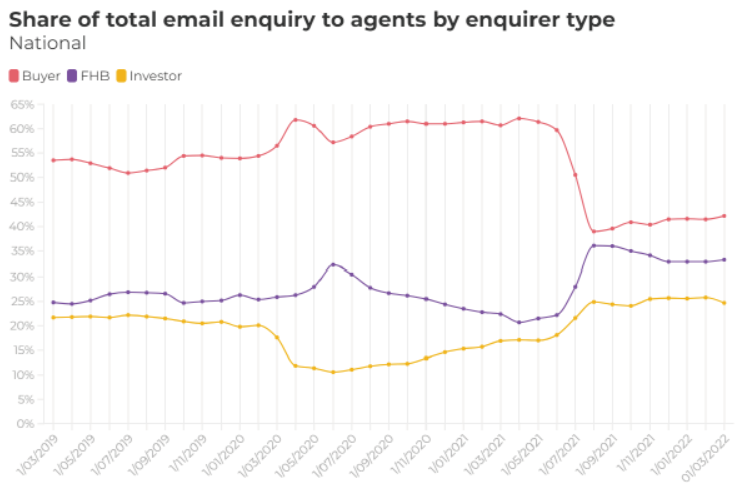

In terms of the share of enquiry, houses remain the dominant type of property enquired about (58.6%), followed by units (32.8%), and then land (8.6%).

The unit share of enquiry continues to increase. In March, the share of enquiry was the highest it’s been (32.8%) since the onset of the pandemic in March 2020.

The premium of house prices over unit prices reached record highs, with the pandemic driving one of the biggest shifts we’ve ever seen when it comes to housing preferences. But with credit conditions tightening and a normalisation of migration placing renewed pressure on inner city rental markets, the share of enquiry is increasing as prospective buyers (owner-occupiers, investors, and first-home buyers) look for more affordable options.

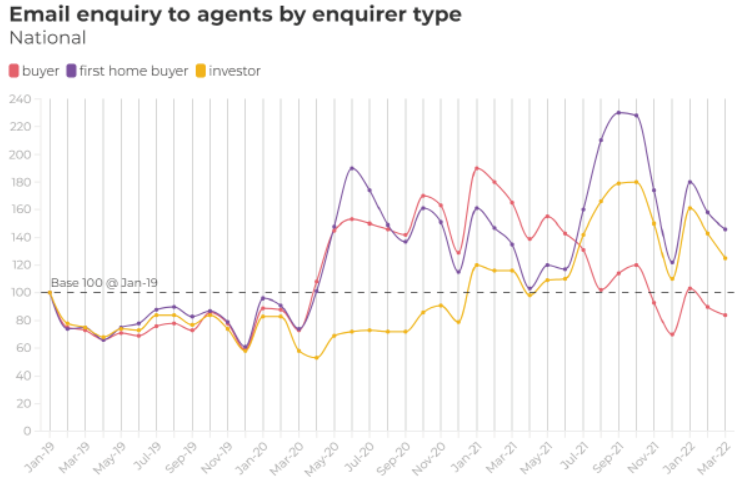

Interest from investors and first-home buyers remains above pre-pandemic levels while owner-occupier enquiry slips

The volume of enquiries to real estate agents from all buyer types continued to slip in March 2022, falling 8.6% month-on- month from February’s levels.

Overall, enquiry volumes for all buyer types have fallen 26.5% year-on-year. Given property seekers can turn-up for inspections in-person now in all states, this high base effect is a likely factor behind slowing email enquiry.

Enquiry volumes from property seekers identifying as owner-occupier buyers fell 7.1% last month to be 49.0% lower than a year earlier. Enquiry volumes also fell throughout March among those identifying as first-home buyers (down 7.5%) and investors (down 12.5%), but remain above levels seen in March 2021 and levels recorded prior to the onset of the pandemic.

First-home buyer enquiry in March 2022 was 8.8% higher than in March last year but has fallen 36.3% from the peak recorded in September 2021. This is to be expected as incentives expire, and higher house prices increase the deposit hurdle for first-timers.

According to the Australian Bureau of Statistics, lending to first-home buyers has also tapered from strong levels recorded in 2021. Again, this is to be expected given the largest barrier to affordability is not servicing debt but challenges saving a deposit.

Nonetheless, first-home buyers remain active relative to pre-pandemic levels, and the volume of enquiry is a little more than 1.5 times the average.

Meanwhile the volume of enquiry from owner-occupier buyers has slipped, down 4.4% from pre-pandemic levels, but investor enquiry is also higher, remaining at 1.5 times pre-pandemic levels.

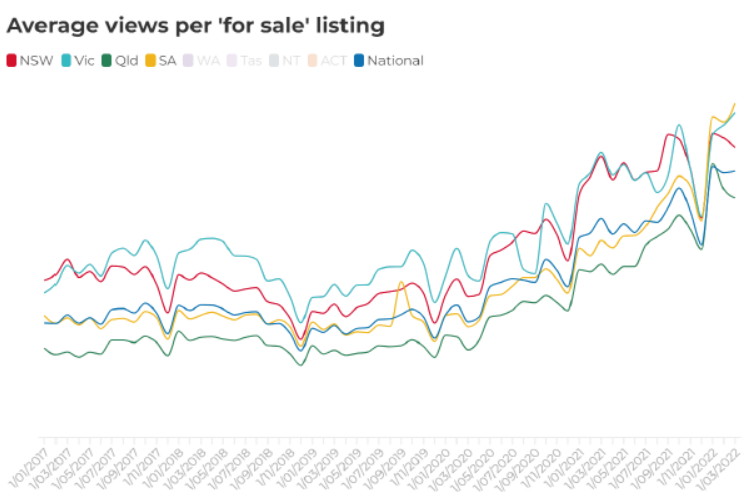

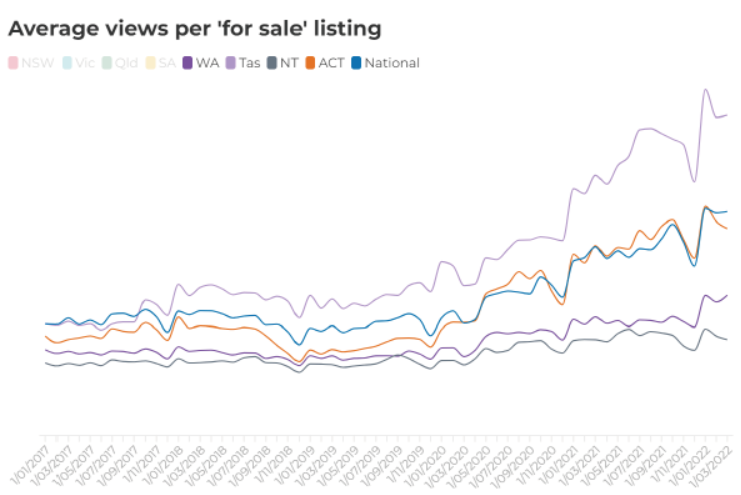

Views per listing fell over the month but remain above average levels

Record high views per listing for much of last year reflected both very high interest from buyers and the relatively low volume of stock available for sale, particularly in regional areas.

The good news for buyers is that we have continued to see more stock for sale coming to market since spring last year. This increased choice continues to ease the prior consistent growth in views per listing.

In March 2022, views per listing fell 1.2% month-on-month to now sit 1.8% lower than January 2022’s record high. Although, nationwide, views per listing are still 24.3% higher than they were this time last year.

Demand based on the number of views per listing on realestate.com.au is still strong right across the country but has moderated from historic highs in all states except Victoria, SA, and WA. In Victoria, views per listing rose 2.7% month-on-month to hit a new historic high in March, now 15.2% higher than levels recorded in March last year.

Views per listing are also at a record high in Melbourne after rising 3.2% month-on-month. In regional Victoria, they have moderated 10.9% off record highs. In Adelaide, views per listing have also hit a new record after climbing 2.9% month-on-month in March 2022, to sit 64.6% higher than this same period last year.

The largest monthly declines in views per listing were recorded in the Northern Territory (down 8.6%), Queensland (down 6.1%), ACT (down 5.9%), and NSW (down 5.1%).

Despite the recent moderation in views per listing, in every GCCSA region except Greater Sydney, views per listing remain above levels recorded in the same period last year. In Sydney, the normalisation of stock available on market and strength in new listings are easing the demand/supply imbalance that characterised much of last year. Views per listing are now 8% lower year-on-year after slipping 3.2% in March 2022.

Views per listing have seen the largest year-on-year uptick in regional SA (90.7%), Adelaide (+64.6%), and regional Queensland (49.3%).

We expect that views per listing are likely to continue moderating off historic high levels, with a larger volume of new stock coming to the market.

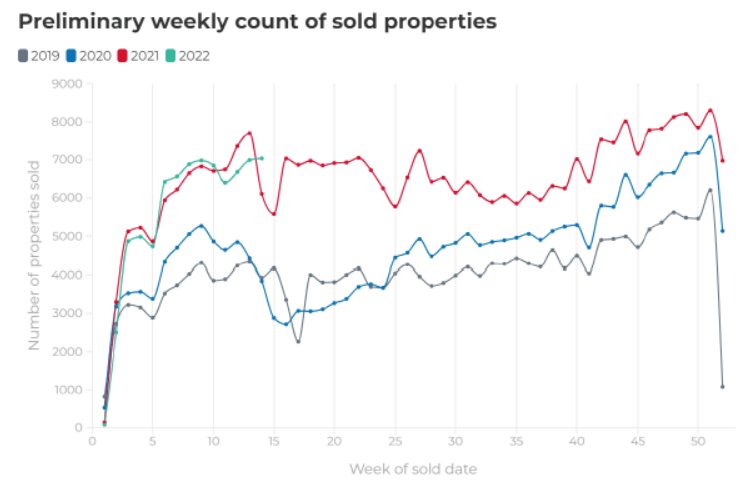

Sales volumes have fallen from record levels but are keeping pace with 2021 so far

Nationally, sales volumes are tracking at a very similar pace to the first 14 weeks of 2021, but the total number of sales has fallen from peak volumes recorded in December 2021.

Preliminary weekly sales volumes so far this year are just 1% lower than over the same period in 2021, and remain 39% higher than the same period in 2020. Many people are expecting that interest rates will rise later this year, which is likely generating some urgency from both buyers and sellers.

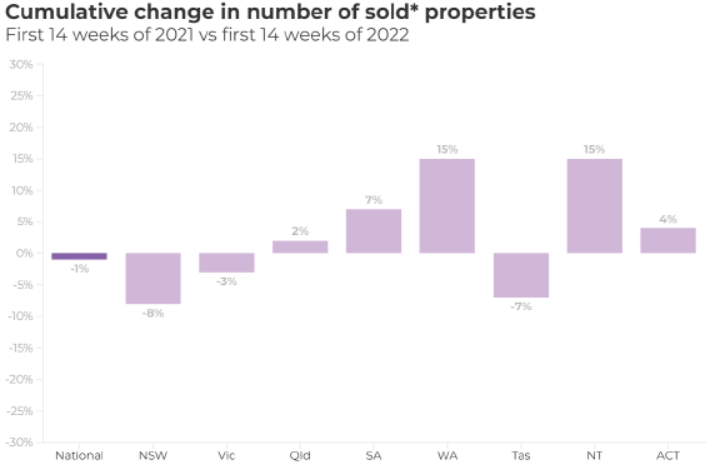

However, not every state is keeping pace with last year’s volumes of preliminary sales. To date this year, sales volumes are off to a slower start compared to the same period last year in Victoria (down 3%), Tasmania (down 7%) and NSW (down 8%).

However, they are outpacing the same period to date last year in the ACT (4%), NT (15%), Queensland (2%), SA (7%), and WA (15%). Sales volumes have most significantly gathered pace in the capital cities of Perth, Adelaide, Brisbane, and Darwin.

Brisbane and Adelaide are seeing demand remaining stronger than in the larger capital cities, boosted by a relative affordability advantage and strong interstate demand. WA is seeing a flurry of activity on the back of eased border restrictions. The state economy continues to fire on all cylinders, fuelling demand from workers for housing, with rental market conditions remaining tight.

Australia-wide, sales volumes in March 2022 were 5.6% lower than March last year. Breaking this down by state, there is some considerable divergence. In WA, NT, and SA, sales volumes are higher than the same period a year ago by 16.3%, 13.3% and 9.9% respectively. In NSW and Victoria, sales volumes are down year-on-year by 13.9% and 6.5% respectively.

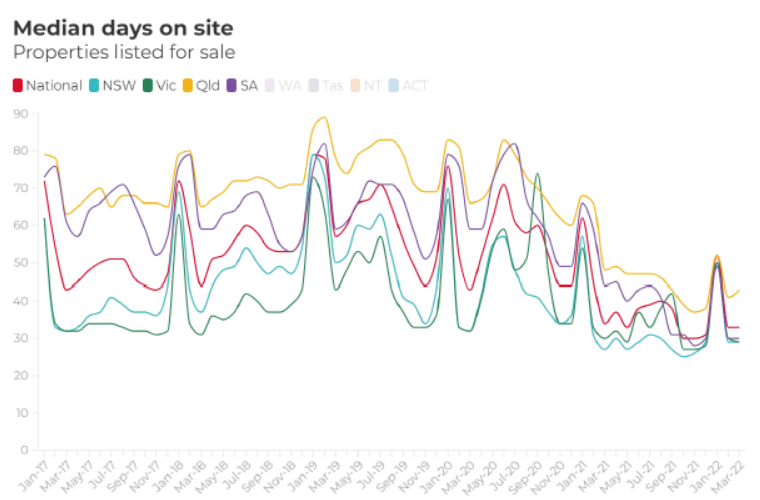

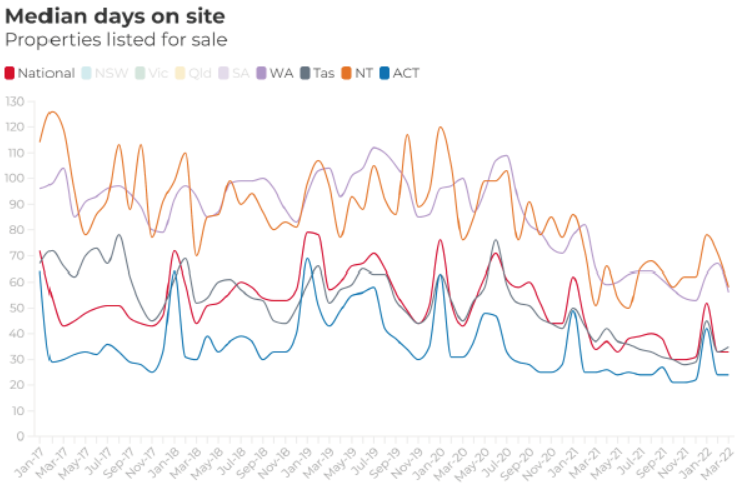

Properties are selling quickly across the country

The median number of days a property was listed on realestate.com.au in March 2022 was 33 days, down from 35 days in February.

Days on site have climbed from the historic low levels experienced last year in every GCCSA region, but properties in most are still selling more quickly than they were in March last year, except in Sydney, Melbourne, Hobart, and Darwin.

In every state’s regional territory, properties are selling more quickly than in March 2021.

Nationally, properties listed for sale spent one day less on site in March 2022 compared to March 2021. The big stand outs are regional SA and regional NT, where the time properties are listed for sale on site has fallen by 73 days and 75 days respectively compared to the same period a year ago. Properties in both saw time on site falling 60 days and 18 days respectively in March 2022.

Throughout March, the largest falls in time on site compared to February were recorded in NT (down 25 days), WA (down 15 days), and Queensland (down seven days). Properties in the ACT continued to sell quickest in March 2022, averaging just 24 days on site.

We do expect that a greater willingness from sellers to list their properties this year should mean more choice and an improved balance between supply and demand.

We have seen the strength in new listings and auction volumes of late 2021 carry over into early 2022. Some of this is likely due to the disruption to sellers’ plans during last year’s lockdowns, while others are thinking this is the time to sell given recent price growth, elevated demand and looming interest rate rises. With more supply and fewer competing bidders, days on site are expected to climb as the year progresses.

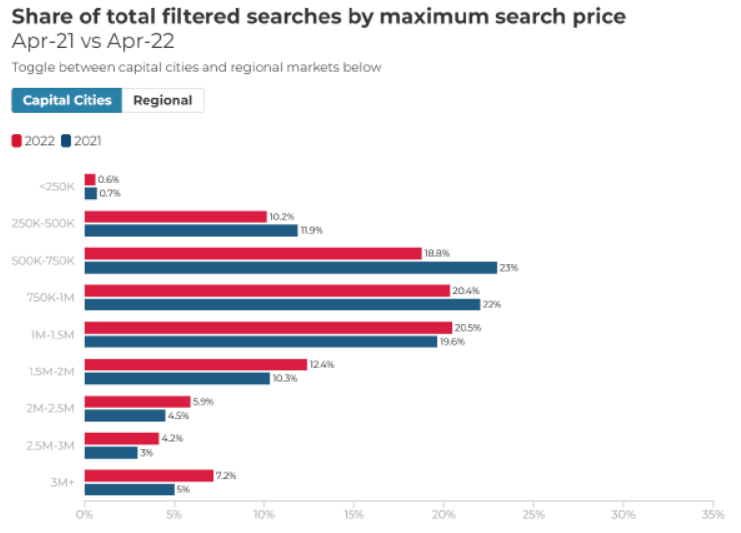

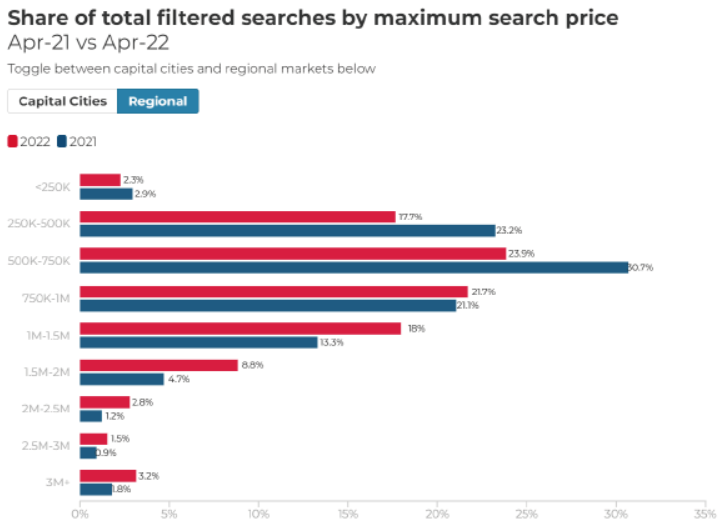

Higher priced property searches continue to increase in popularity

The fastest annual pace of price growth in more than three decades has meant that prospective buyers are looking at higher price points.

Throughout the combined capital cities, 50.1% of searches in March 2022 were for properties listed at a price over $1 million, up 0.4 percentage points from February. A year ago, that share was 42.3%.

Buyers looking to purchase in regional areas are still searching for more affordable properties compared to capital cities but even so the share of searches for regional properties listed at more than $1 million has almost tripled since the onset of the pandemic. This increased a further 1.1 percentage point in March to reach 34.3%, compared to just 21.9% a year ago.

Throughout the combined capital cities in January 2022, 39.1% of searches were for properties listed at a price between $500,000 and $1 million, compared to 45.2% a year earlier.

Unsurprisingly, the increase in dwelling prices and higher priced searches have seen a large decline in the share of searches under $500,000. Between March 2021 and March 2022 there has been a drop in searches for sub-$500,000 properties, both in capital cities and regional areas. In March 2022, just 10.8% of capital city searches were for properties listed below $500,000 compared to 12.6% a year earlier. In February 2020, that share was 16.5%.

In regional areas, searches under $500,000 have fallen to 19.9%, down from 26.2% a year ago.

Demand from prospective property purchasers has moderated but remains strong, and borrowing costs remain low, despite fixed rates having begun to climb. The pace of price growth is moderating but it would be reasonable to expect a further increase in higher priced searches as the hottest property market in decades has pushed housing prices higher Australia-wide.

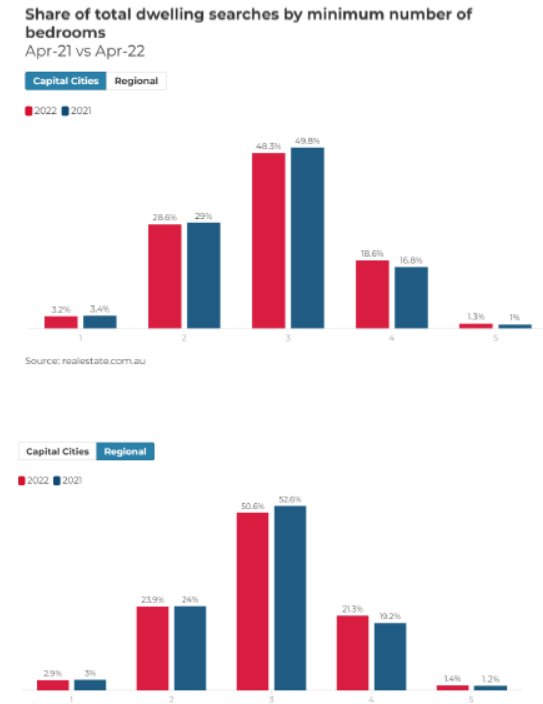

Property seekers continue to scope out homes with three or more bedrooms

The majority of property seekers continue to search for a minimum of three bedrooms.

In March 2022, 68.2% of filtered searches on realestate.com.au across the capital cities were for a minimum of three bedrooms.

This trend is also playing out in regional areas, where 73.2% of filtered searches were for a minimum of three bedrooms, up 0.5 percentage points from February and up from the 72.9% share seen in March last year.

Space will continue to be an important factor for many buyers despite price rises, and we expect demand for larger properties will likely remain substantial given the experience of lockdowns and the COVID-19 induced preference shift towards larger homes, for both working from home and lifestyle reasons.

However, with investor activity on the rise, we may see renewed interest in smaller dwellings, particularly in capital cities.