Investment Climate

Conditions remain positive for real estate

Conditions for real estate are expected to remain positive over the next year. Although COVID-19 remains present in the community, the economic effects going forward should be mitigated by high vaccination rates and the easing of international travel restrictions. The Ukraine conflict has been a two-edged sword, both adding to domestic inflationary pressures and increasing the value of exports.

Our key assumptions are:

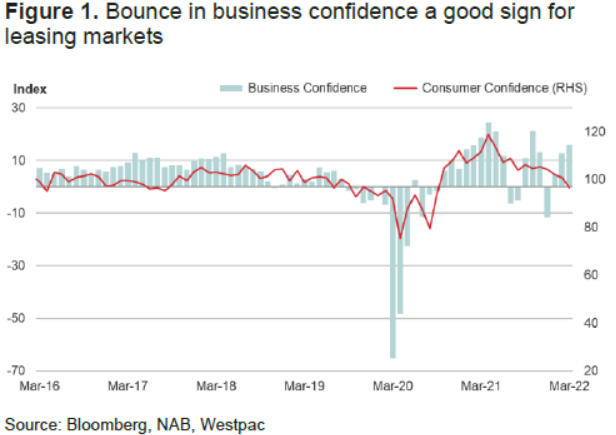

– Business confidence to remain resilient but consumer confidence weighed down by the prospect of higher interest rates (Figure 1).

– Housing and infrastructure construction will positively contribute to growth albeit rising construction costs make return on investment less certain.

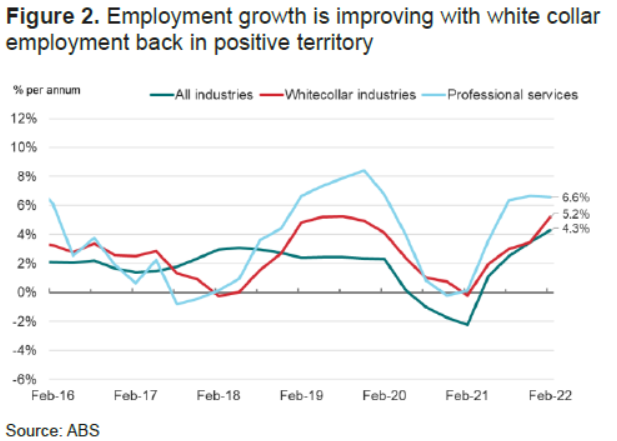

– Employment trends are positive, albeit the data are somewhat skewed by absence of overseas workers (Figure 2).

– Retail spending will continue to grow, largely from accumulated savings.

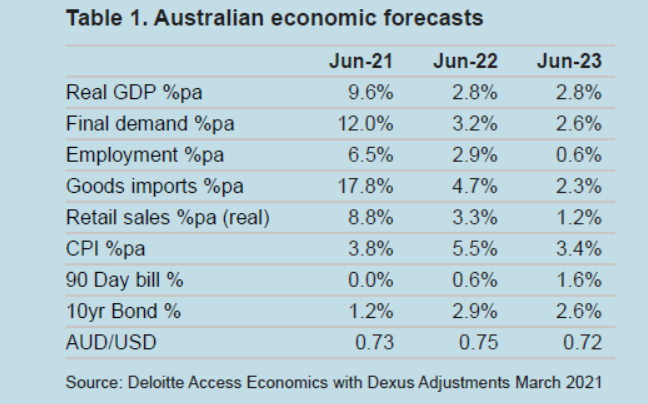

– Short-term interest rates will rise in FY23 to circa 1.5%. Long term yields are likely to be more stable, being already at 3.0%.

The main themes to consider in FY23 are:

– Construction costs are likely to rise further over the next year given no respite to inflationary pressures or supply chain disruptions so far;

– Short-term growth prospects in the industrial and healthcare sectors are better than for office and retail, where vacancy will take time to absorb; and

– Capital flows into property are likely to remain solid given significant investor appetite, however a rising cost of capital may curb price expectations.

Construction cost outlook

A more complex development equation

Construction costs have risen sharply over the past year, putting pressure on the margins of construction companies and their subcontractors and increasing the cost of development. The uncertainty of future cost increases has led to construction companies reverting to shorter tender validity periods, and it has sharpened negotiations around contracts in order to allow for rises or falls in the cost of components. For developers it has meant a review of contingencies.

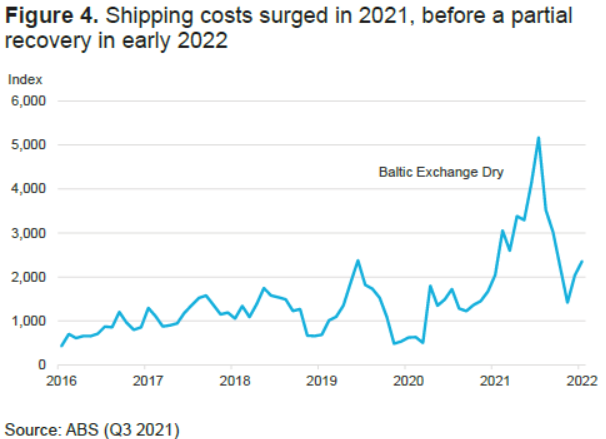

The lift in construction costs can largely be attributed to the pandemic. Pandemic-induced government stimulus to the construction sector at a time when COVID-19 disrupted international supply chains has led to shortages of some materials, particularly when imported. Shipping costs have risen substantially due to supply chain bottlenecks (Figure 4). Increases in demand globally have placed pressure on international freight capacity. Lockdowns in major port cities such has Shanghai have exacerbated bottlenecks.

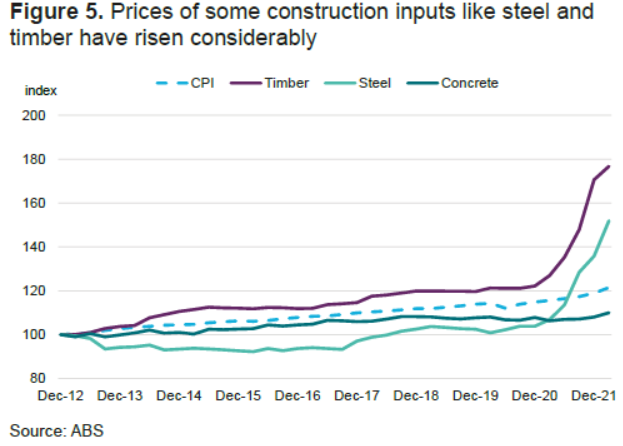

These events have put upward pressure on input costs for construction. Timber prices have risen 39% year on year, while steel prices, including for reinforcing, have risen by 42% (Figure 5). Steel fittings are similarly affected. Other materials like concrete have been less affected, particularly where domestically sourced. This increase in input costs have a flow-on impact to tender prices.

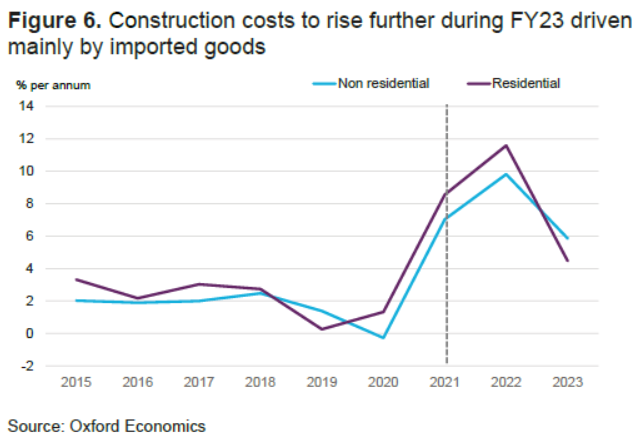

Given many of the cost increases are related to one-off disruptions it is anticipated that they will ease over time. However, the time frame for this reversion is uncertain, particularly as the pandemic and Ukraine conflict are still in progress and infrastructure construction is running at high levels. Consequently, the most likely outlook, reflected in the Oxford Economics forecast (Figure 6), is that construction costs will continue to rise in at above average pace in FY23 before normalising through FY24 and FY25.

Performance and transactions

Real estate performing solidly in 2022

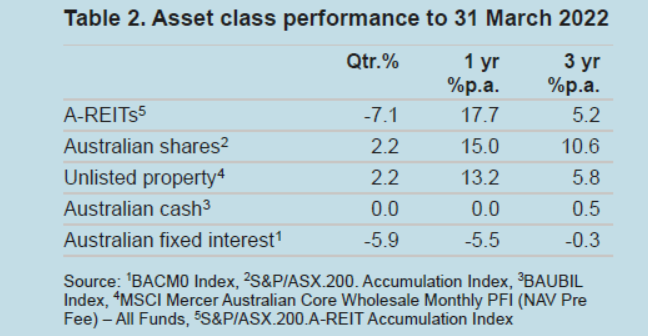

The ASX 200 A-REIT index (+13.5%) has outperformed the ASX S&P 200 Index (+10.4%) in the year to Q1 2022. While returns were positive overall in Q1, the A-REIT index pulled back in March as 10 year bond yields increased sharply from 2.1% to 2.8% in the month. While bond yields have risen, they are still low in historical terms and similar to the trading levels seen between 2015 and 2019.

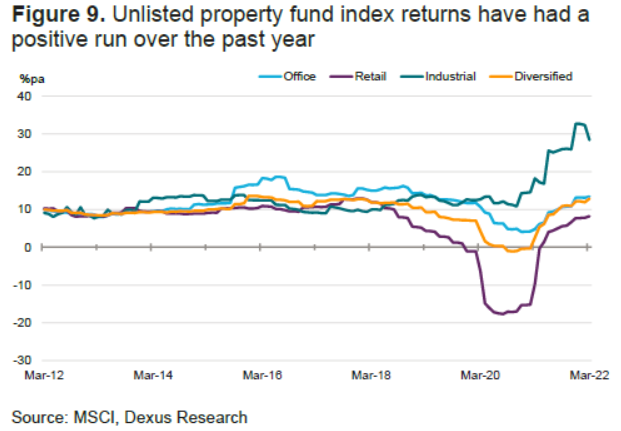

Unlisted funds have performed solidly over the quarter after a year of recovery with diversified funds returning 12.9% per annum. Industrial funds (28.4%) significantly outperformed the other sectors over the past year, followed by office (13.4%). Retail returns strengthened to 8.2% for the year, reflecting a firming of capital values.

Transaction volumes in Q1 2022 were comparable to Q1 last year. There was a lift in non-CBD office deals (sub 15,000sqm buildings) with an interest from domestic capital. Foreign demand for high quality CBD assets also remained robust particularly in the Sydney CBD. Blackstone continued their expansion in Australian real estate with the purchase of Grosvenor Place for $465m.

Momentum in the industrial sector continued in Q1 2022 with $2.0bn worth of transactions, lifting the 12 month total to $20.3bn. The majority of activity was in the Sydney market, with a sharp focus on strategic infill locations benefiting from ecommerce fulfilment. ESR acquired a 77,000sqm at 270-286 Horsley Road, Milperra for $152m in close proximity to Bankstown Airport.

Retail transactions increased during 2021 as investor sentiment improved. Sentiment remains weak overall, but is more positive for smaller supermarket based centres than for larger discretionary centres. Accordingly, pricing has tightened for the smaller centres. Larger centres now offer a more attractive yield and several of them have traded in recent times with demand driven by domestic investors focusing on a sustainable growth story and any mixed use potential.

Office

Smaller occupiers driving office recovery

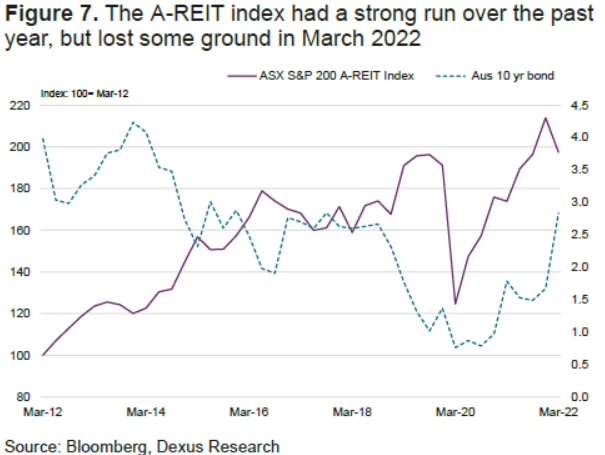

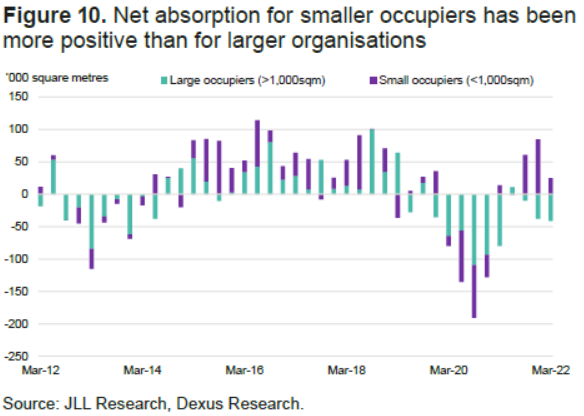

After three positive quarters, net absorption for the four major CBDs eased in Q1 2022. The decline can be attributed to a few large organisations either contracting or offering sublease space in Sydney and Melbourne. On a positive note, smaller occupiers have remained active across all CBD markets, being able to make decisions quicker and with less legacy cost pressures (Figure 7).

Leasing enquiry data has been positive with the number of active tenant briefs rising to pre-pandemic levels. Larger organisations are becoming more active in the pre-commitment market, with several new leases being signed on new developments. Most promisingly, many organisations are committing to more space than before and signaling a preference for prime quality space.

While physical occupancy rates remain low, workers are starting to make their way back into CBDs as more offices open. There remains a discrepancy in employee and employer expectations regarding the frequency with which staff will be in the office. Physical occupancy was recorded at 41% in Sydney CBD and 32% in Melbourne CBD, though foot traffic varies greatly within precincts in office markets.

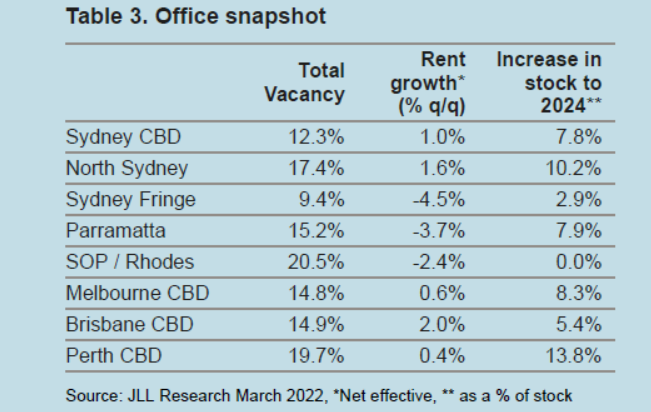

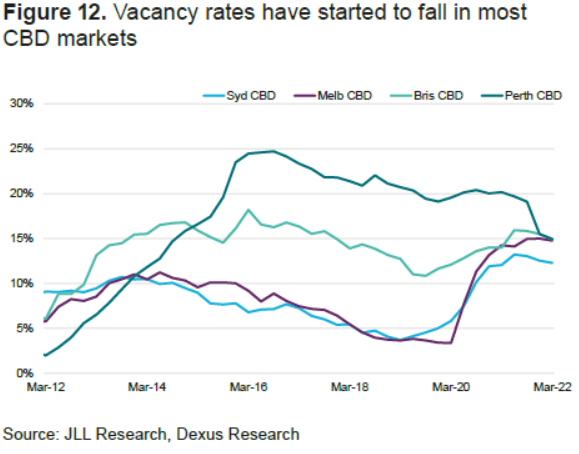

Vacancy rates appear to have turned the corner, falling in Sydney CBD and Melbourne CBD in the March quarter, mainly due to stock withdrawals. Sub-lease vacancy also fell in both markets (1.7% and 2.6% respectively) as companies took back space. There is also a notable difference in vacancy rates across precincts, with Sydney’s Core having significantly less vacant space (10.5%) than the city’s other precincts, indicating that occupiers prefer areas with greater amenity. Vacancy in the Brisbane and Perth CBDs also fell, with larger occupiers driving momentum in these markets.

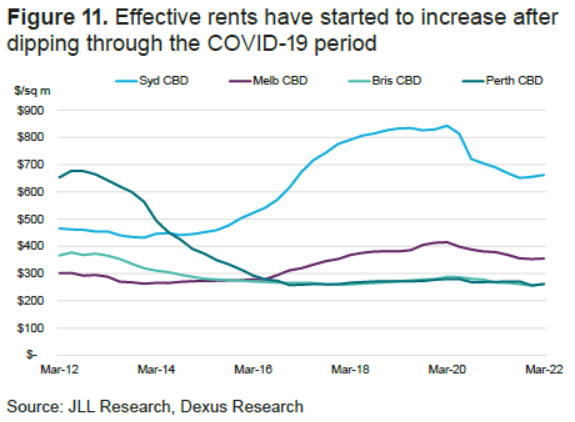

Effective rents rose across all CBD markets as face rents rose, although incentives remain elevated. Yields in Sydney and Melbourne fell 10 basis points in Q1 2022, while staying flat in Perth and Brisbane.

Industrial

Strong rent growth story

The Australian industrial sector is well positioned for another year of strong performance. Supply chain investment by retailers and continued growth in ecommerce is resulting in record levels of take-up. Existing assets are benefiting from falling vacancy rates and the need for new stock is supporting high levels of development.

Demand for industrial space continues to remain at elevated levels with 800,000sqm absorbed over the past quarter. The Sydney and Melbourne markets enjoyed a strong start to the year, together accounting for three quarters of national demand. Pre-lease activity was the main driver of take-up across both markets reflecting 95% and 62% respectfully.

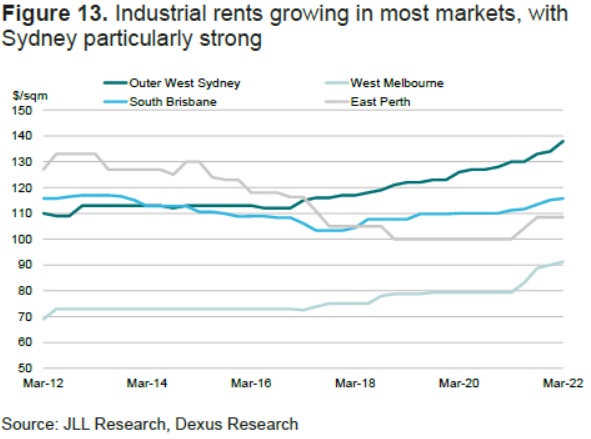

The immediate outlook for rent growth looks strong with South-East Melbourne recording the strongest quarterly growth at +7.9% according to JLL. All Sydney markets experienced substantial growth with the South-West jumping a further 5.6%.

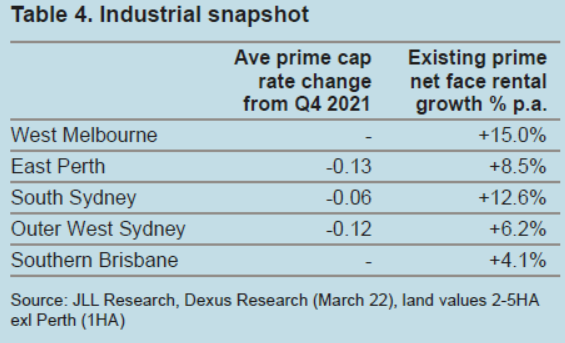

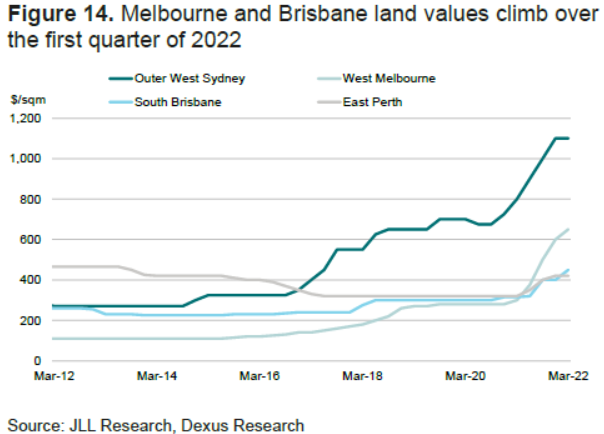

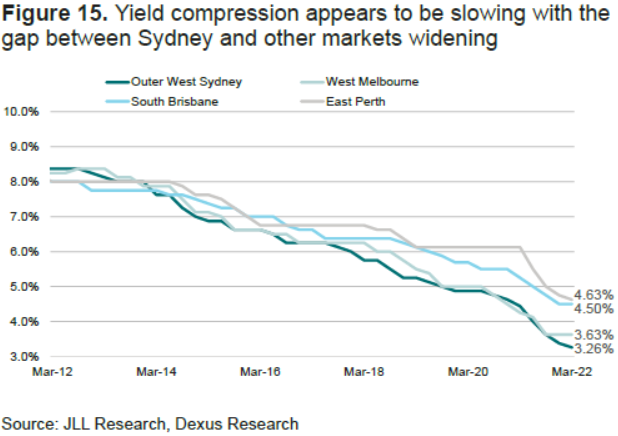

Rising development costs are expected to add to pressures for rental growth. In FY22, industrial construction tender prices are estimated to have risen by more than 10% and land values in West Melbourne have doubled. In the past few years, rents have been shielded from rising land values and construction costs by yield compression, which underpinned values and allowed supply to come to market at a competitive rent level. Looking forward, if the rate of yield compression slows, rising development costs will have to flow through to higher pre-commitment rents.

There continues to be a significant weight of capital looking to gain exposure to the industrial sector. Over the quarter around $2bn entered the industrial market, $400m above this time last year. Sydney land fetched the highest transaction value with 1 Augusta Street, Huntingwood for $201m ($928/sqm) and Badgerys Creek Aerotropolis for $140m ($583/sqm). The rate of yield compression appears to be slowing. Average prime Sydney Yields tightened a further 12bps across the board whereas Melbourne and Brisbane remained steady.

Industrial by region

Outer West Sydney

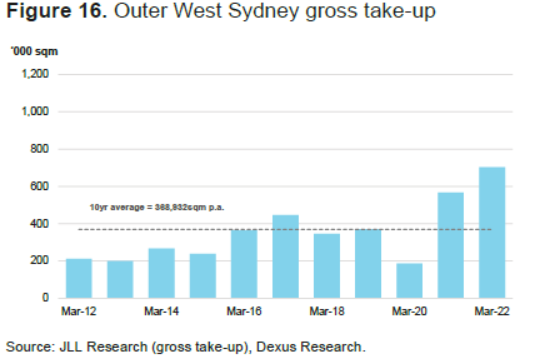

Take-up levels in the Outer West Sydney market were broadly in line with last year with, 150,000sqm absorbed. The Outer West Sydney precinct continues to benefit from strong pre-leasing activity. Mirvac welcomed two new signings to their Aspect industrial estate in the Kemps Creek precinct with Winning Appliances (66,000sqm) at $116/sqm and a 34% incentive and Lineage Logistics in 36,000sqm. Although incentives do appear to be falling across the broader Outer West market, competition within the Kemps Creek precinct looks to weigh on effective rents in the wake of supply.

West Melbourne

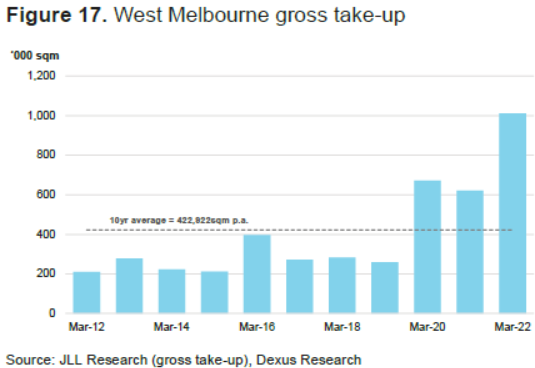

Quarterly take-up volumes in West Melbourne recorded a solid 206,000sqm after a record breaking 2021 calendar year. Logistics was the major driver of demand accounting for around 40% of take-up, with a pull towards new supply. Charter Hall signed DSV to their recently completed Warehouse 3 within Midwest Logistics Hub while TMA pre-leased Cabot’s 14,000sqm at 8 Market Place, Truganina. The West Melbourne market continues to benefit from a significant imbalance between supply and demand with around 77% of supply under construction already committed for 2022.

Brisbane (South & Australian Trade Coast)

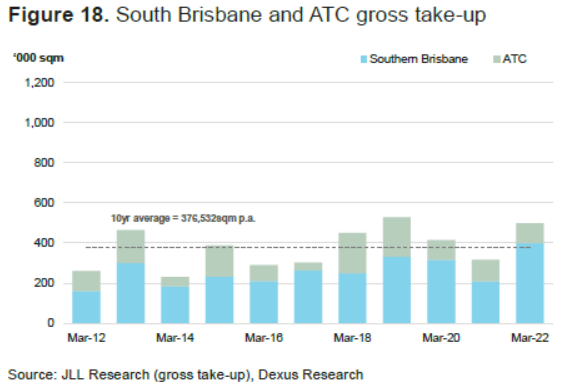

The Brisbane market started the calendar year broadly in line with last year with around 108,000sqm absorbed between the South and Trade Coast. Leasing activity has been consistent around the Trade Coast with circa 20,000-30,000sqm absorbed per quarter, driven by the Port/Airport precincts. Within the South, Dexus welcomed Linfox to Warehouse 4 at the newly built Freeman Central, Richlands. The Brisbane leasing market continues to be influenced by a large degree of supply under construction in the South, with 60% being speculatively developed (PC 2022). Looking forward, this is likely to have a material impact on effective rents.

Perth (East & South)

Take-up within the Perth industrial market cooled off after a strong 2021, with 11,300sqm absorbed over the quarter. Leasing volumes were thin with three sub- 5,000sqm deals within Henderson in the South and Hazelmere/Forrestfield to the East. The Perth market represents an attractive investment opportunity with a circa 120bbps yields spread to Sydney/Melbourne industrial. Existing prime rents in South Perth continued to gather momentum over the quarter climbing another 3% to $100/sqm representing 8.2% growth year on year.

Retail

Retail sales continue to grow

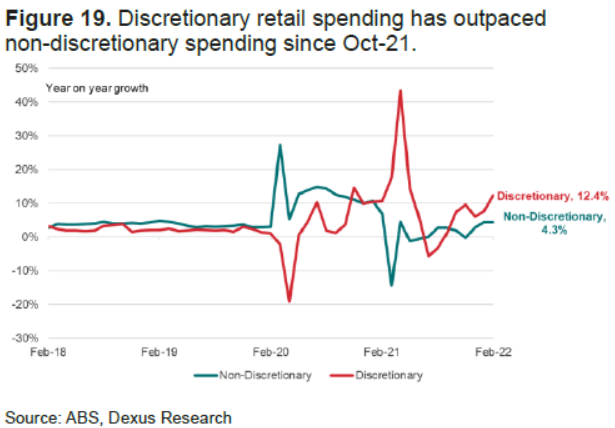

Retail sales increased by 5.3% in moving annual terms in the year to February 2022. This above average level of sales has been driven by a catch up in a discretionary spending. Sales in discretionary categories such as clothing, cafes restaurants and takeaways have significantly outpaced grocery store sales volumes over the past year (Figure 19). Spending is being supported by a tight labour market, low interest rates and a high savings rate.

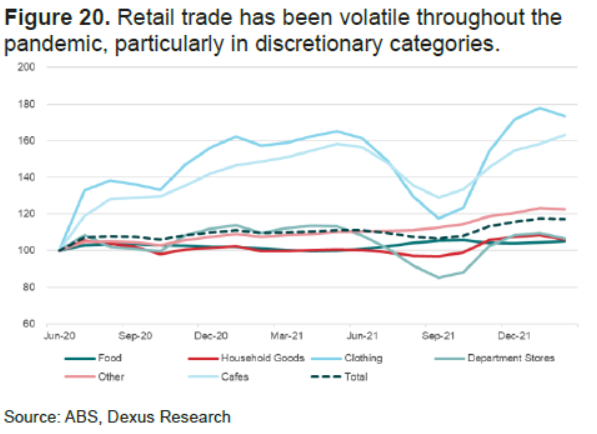

Shopping centres performance is slowly improving, but they have not been able to capitalise on all the spending growth during the COVID-19 period. For example, much of the spending in the household goods category was in standalone and bulky goods premises such as Bunnings, Officeworks and Harvey Norman. Smaller centres anchored by supermarkets performed best, given their reliance on non-discretionary spending. While large regional centres have borne the brunt of the pandemic (Figure 21). As discretionary spending continues to improve, centres with more discretionary style tenants (often larger centres), will benefit from the rebalancing of retail trade to more normal patterns.

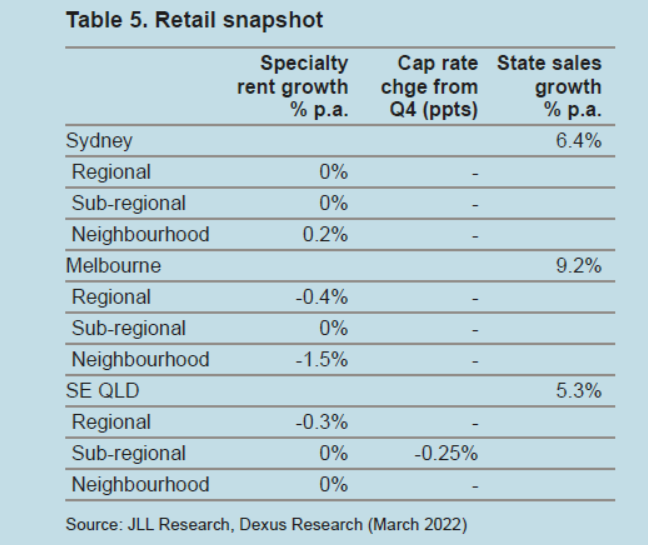

The March quarter saw rents stabilise across shopping centres nationally according to JLL (and noting that there is wide variation between individual centres). Rents were steady for regional and subregional shopping centres, with a marginal fall in neighbourhood shopping centres.

City retail remains challenged given the pandemic’s effects on CBD locations and the number of store closures. City centres are recovering, but it will take time, and depend on the rate of return of office workers and tourists. However, FY23 should be a year of upside from a low base as office workers, tourists and university students return.

Healthcare

Increasing merger and acquisition activity

Mergers, acquisitions, and joint ventures are becoming increasingly common in the healthcare sector, as investors contend with a more competitive investment market. Limited available assets are seeing large real estate owners and fund managers work together to increase their buying power. Additionally, there is growing investment in the development of health precincts, with sites being acquired specifically for such developments.

Of note, the recent Centuria and Morgan Stanley Real Estate Investing partnership highlights an alternative method of entry into the Australian healthcare property market – being the recapitalisation of an existing Centuria healthcare vehicle with Grosvenor.

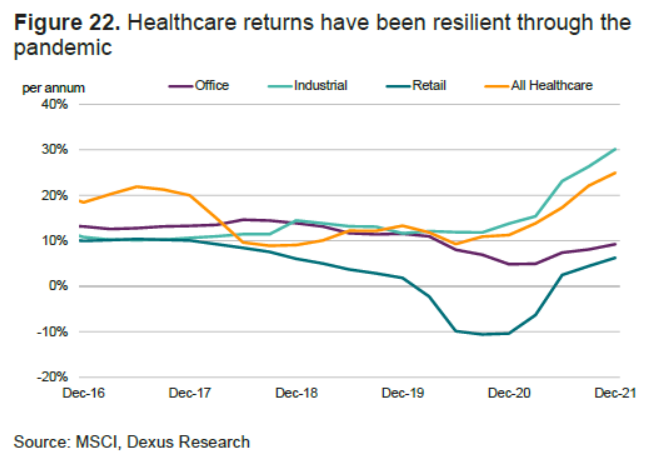

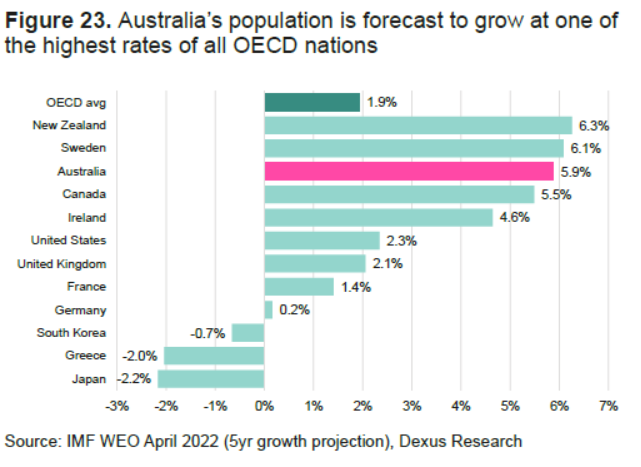

Institutional owners targeting healthcare assets are increasingly focusing their attention in high-growth suburban areas of capital cities. These are areas that are set to benefit from high levels of population growth, have favourable demographics and high levels of infrastructure activity. Longer life expectancies, a more aged population, growing demand for medical services and increasing government investment into the sector are all proving to be strong tailwinds for investment into healthcare real estate. Indeed, Australia’s population growth forecasts are among the highest of all OECD nations (Figure 2).

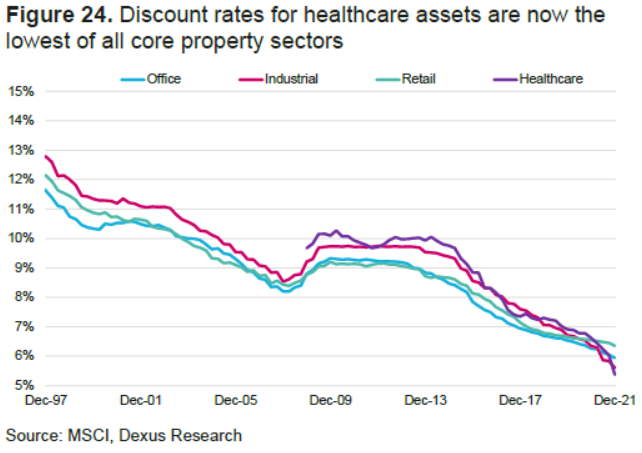

This strong investment demand is now reflected in healthcare pricing, with discount rates for healthcare assets now the lowest of all core property sectors (Figure 3); 5.4% for healthcare versus 5.6% for industrial. There is also very little differential between the healthcare sub-sectors, with cap rates for medical centres (4.6%) only marginally higher than hospitals (4.5%), indicating strong competition for all types of assets. While institutional investors are driving demand for larger assets with development potential, smaller private investors looking to diversify into the healthcare sector, are more active in the transaction of medical centres, driving cap rates lower.

Amid the current competitive environment, quality is becoming even more important, to secure stable longterm income streams. As healthcare becomes more institutionalised, the focus on the quality of tenants is growing, with the most sought after properties being those that are secured by larger tenants who have long-standing and propitious terms with health insurers, in trade areas with favourable demographics. These sorts of businesses usually have high set-up costs that act as a barrier to entry, reducing competition.